Florida Multi-Family Mortgage Lenders

Yes, we offer no-personal-income investor loans in Florida. Our Florida mortgage lenders offer loans for Single-family, Multifamily, Pad split, 2-4-unit, and condo properties. Our no-income-verification Florida mortgage lenders provide financing for a type of commercial real estate loan used to purchase, refinance, or rehabilitate properties with five or more residential units. Florida multifamily properties can include apartment buildings, townhouses, and other multi-unit dwellings.

NoTax Return Mortgage Programs Include:

- Home Loan No Tax Returns =OK 1099 mortgage Lenders = OK 3 Months Bank Statement = OK

- Self-Employed Less than 1 year = OK VOE Only Mortgage = OK Asset Depletion = OK

- ITIN No Tax return mortgage = OK Nonresident No Tax Return = OK Pledged Assets = OK

- Asset Depletion or Pledged = OK Business Profit Loss = OK DSCR Rental Income = OK

- No Doc, No W2, No Tax Return = OK Bank Statement Deposits = OK Jumbo No Tax Returns = OK

- NO Tax Return Short Term Rental = OK No Income Investor Refinance = OK Condo Refi No Tax Returns = OK

- Estate Refinance NO Tax Return = OK No Income Refinance = OK Condo Cashout No Tax Returns = OK

No Income Verification Florida Investor loans

Padsplit Florida Mortgage Lenders

Florida mortgage lenders now offer pad-split mortgage programs for Florida investors who rent rooms in properties. These loans are available for affordable, private rent-by-the-room rentals throughout Florida and can finance 1-4 family pad-split homes as well as mixed-use properties suitable for the Padsplit model. No personal income verification is required for qualification; instead, current pad-split rental income can be used to secure financing. Florida Padsplit mortgage lenders also provide options for both cash-out refinances and purchases of Padsplit homes in any city. These programs help Florida investors tap into the growing co-living market with flexible terms, competitive rates, and innovative qualification methods for Padsplit-approved properties.

Cashout Refinance Florida Padsplit

NO Income Verification Investor Loans Florida

No Income Verification Florida Investor Loans

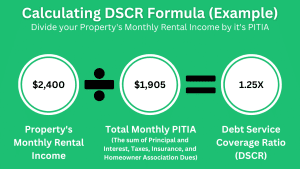

Debt Service Coverage Ratio (DSCR): Florida no-income-verification mortgage lenders often use DSCR to assess a property’s ability to cover its debt obligations. It’s calculated by dividing the property’s net operating income (NOI) by its total debt service (principal and interest payments). A DSCR greater than 1.0 indicates the property generates enough income to cover all of its monthly obligations, including principal, interest, taxes, and insurance.

PadSplit Rent By The Room Mortgage Lenders:

Florida properties listed through PadSplit’s marketplace are eligible with the following requirements:

• 70% LTV Max

• Refinance

• Income Documentation directly from PadSplit.com required

• Qualifying income is the most recent 12-month average

• Properties can’t have a bedroom count higher than exists in the market for the square footage

• Bedroom occupancy max must be legal per zoning

• Property must be C3 or better condition

• Non PadSplit single room occupancy properties are ineligible

Mutil Family Florida Mortgage Key Features:

Commercial Loan: Unlike residential Florida mortgages for single-family homes, multifamily mortgages are considered commercial loans. This means the underwriting process, terms, and regulations can vary.

Number of Units: The property must have at least 5 units. Florida multifamily properties with 2 to 4 units are often financed with residential mortgages.

Loan Purposes: Multifamily mortgages can be used for various purposes:

Acquisition: To purchase an existing multifamily property.

Refinance: To replace an existing mortgage with a new one, potentially to lower interest rates, change loan terms, or access equity.

Rehabilitation: To finance significant renovations or improvements to an existing property.

Borrower: Borrowers are typically real estate investors, developers, or property management companies rather than individual homeowners.

Underwriting: Lenders assess the borrower’s financial health, experience, and the property’s income-generating potential (rental income) to determine loan eligibility and terms. Factors like occupancy rates, rental income, and operating expenses are crucial.

Loan Terms: Loan terms can vary significantly based on the lender, loan type, and market conditions. They can include fixed or adjustable interest rates, and amortization schedules that can extend up to 30 years or more.

Loan-to-Value (LTV): Lenders typically have a maximum LTV of 80%, based on credit, reserves, and DSCR, meaning they will finance only a certain percentage of the property’s value. Borrowers need to provide a down payment, which can vary depending on the overall loan characteristics.

Multifamily Florida Mortgage Lenders

Provides developers with gap financing to secure full financing for affordable rental housing.

Makes low or no-interest, non-amortizing loans to developers who acquire, rehabilitate, or construct housing for low-income families.

Provides nonprofit and for-profit developers with a dollar-for-dollar reduction in federal tax liability in exchange for the development of affordable rental housing.

Uses both taxable and tax-exempt bonds to provide below-market-rate construction loans to nonprofit and for-profit developers of affordable housing.

Assists affordable housing developers with up to $750,000 in financing for predevelopment activities associated with the construction of affordable housing, such as rezoning, title searches, impact fees, and other requirements.

| Alachua | Alachua County |

| Alford | Jackson County |

| Altamonte Springs | Seminole County |

| Altha | Calhoun County |

| Anna Maria | Manatee County |

| Apalachicola | Frankin County |

| Apopka | Orange County |

| Arcadia | DeSoto County |

| Archer | Alachua County |

| Astatula | Lake County |

| Atlantic Beach | Duval County |

| Atlantis | Palm Beach County |

| Auburndale | Polk County |

| Aventura | Miami-Dade County |

| Avon Park | Highlands County |

| Bal Harbor | Miami-Dade County |

| Baldwin | Duval County |

| Bartow | Polk County |

| Bascom | Jackson County |

| Bay Harbor Islands | Miami-Dade County |

| Bay Lake | Orange County |

| Bell | Gilchrist County |

| Belle Glade | Palm Beach County |

| Belle Isle | Orange County |

| Belleair | Pinellas County |

| Belleair Beach | Pinellas County |

| Belleair Bluffs | Pinellas County |

| Belleair Shore | Pinellas County |

| Belleview | Marion County |

| Beverly Beach | Flagler County |

| Biscayne Park | Miami-Dade County |

| Blountstown | Calhoun County |

| Boca Raton | Palm Beach County |

| Bonifay | Holmes County |

| Bonita Springs | Lee County |

| Bowling Green | Hardee County |

| Boynton Beach | Palm Beach County |

| Bradenton Beach | Manatee County |

| Bradenton | Manatee County |

| Branford | Suwannee County |

| Briny Breezes | Palm Beach County |

| Bristol | Liberty County |

| Bronson | Levy County |

| Brooker | Bradford County |

| Brooksville | Hernando County |

| Bunnell | Flagler County |

| Bushnell | Sumter County |

| Callahan | Nassau County |

| Callaway | Bay County |

| Cambelton | Jackson County |

| Cape Canaveral | Brevard County |

| Cape Coral | Lee County |

| Carrabelle | Frankin County |

| Caryville | Washington County |

| Casselberry | Seminole County |

| Cedar Grove | Bay County |

| Cedar Key | Levy County |

| Center Hill | Sumter County |

| Century | Escambia County |

| Chattahoochee | Gadsden County |

| Chiefland | Levy County |

| Chipley | Washington County |

| Cinco Bayou | Okaloosa County |

| Clearwater | Pinellas County |

| Clermont | Lake County |

| Clewiston | Hendry County |

| Cloud Lake | Palm Beach County |

| Cocoa | Brevard County |

| Cocoa Beach | Brevard County |

| Coconut Creek | Broward County |

| Coleman | Sumter County |

| Cooper City | Broward County |

| Coral Gables | Miami-Dade County |

| Coral Springs | Broward County |

| Cottondale | Jackson County |

| Crawfordville | Wakulla County |

| Crescent City | Putnam County |

| Crestview | Okaloosa County |

| Cross City | Dixie County |

| Crystal River | Citrus County |

| Dade City | Pasco County |

| Dania Beach | Broward County |

| Davenport | Polk County |

| Davie | Broward County |

| Daytona Beach | Volusia County |

| Daytona Beach Shores | Volusia County |

| DeBary | Volusia County |

| Deerfield Beach | Broward County |

| DeFuniak Springs | Walton County |

| DeLand | Volusia County |

| Delray Beach | Palm Beach County |

| Deltona | Volusia County |

| Destin | Okaloosa County |

| Doral | Miami-Dade County |

| Dundee | Polk County |

| Dunedin | Pinellas County |

| Dunnellon | Marion County |

| Eagle Lake | Polk County |

| Eatonville | Orange County |

| Ebro | Washington County |

| Edgewater | Volusia County |

| Edgewood | Orange County |

| El Portal | Miami-Dade County |

| Esto | Holmes County |

| Eustis | Lake County |

| Everglades City | Collier County |

| Fanning Springs | Gilchrist County |

| Fanning Springs | Levy County |

| Fellsmere | Indian River County |

| Fernandina Beach | Nassau County |

| Flagler Beach | Flagler County |

| Florida City | Miami-Dade County |

| Fort Lauderdale | Broward County |

| Fort Meade | Polk County |

| Fort Myers Beach | Lee County |

| Fort Myers | Lee County |

| Fort Pierce | St. Lucie County |

| Fort Walton Beach | Okaloosa County |

| Fort White | Columbia County |

| Freeport | Walton County |

| Frostproof | Polk County |

| Fruitland Park | Lake County |

| Gainesville | Alachua County |

| Glen Ridge | Palm Beach County |

| Glen Saint Mary | Baker County |

| Golden Beach | Miami-Dade County |

| Golf | Palm Beach County |

| Golfview | Palm Beach County |

| Graceville | Jackson County |

| Grand Ridge | Jackson County |

| Green Cove Springs | Clay County |

| Greenacres | Palm Beach County |

| Greensboro | Gadsden County |

| Greenvilee | Madison County |

| Greenwood | Jackson County |

| Gretna | Gadsden County |

| Groveland | Lake County |

| Gulf Breeze | Santa Rosa County |

| Gulf Stream | Palm Beach County |

| Gulfport | Pinellas County |

| Haines City | Polk County |

| Hallandale | Broward County |

| Hampton Beach | Bradford County |

| Hastings | St. Johns County |

| Havana | Gadsden County |

| Haverhill | Palm Beach County |

| Hawthorne | Alachua County |

| Hialeah | Miami-Dade County |

| Hialeah Gardens | Miami-Dade County |

| High Springs | Alachua County |

| Highland Beach | Palm Beach County |

| Highland Park | Polk County |

| Hillcrest Heights | Polk County |

| Hilliard | Nassau County |

| Hillsboro Beach | Broward County |

| Holly Hill | Volusia County |

| Hollywood | Broward County |

| Holmes Beach | Manatee County |

| Homestead | Miami-Dade County |

| Horseshoe Beach | Dixie County |

| Howey-in-the-Hills | Lake County |

| Hupoluxo | Palm Beach County |

| Indialantic | Brevard County |

| Indian Creek | Miami-Dade County |

| Indian Harbour Beach | Brevard County |

| Indian River Shores | Indian River County |

| Indian Rocks Beach | Pinellas County |

| Indian Shores | Pinellas County |

| Inglis | Levy County |

| Interlachen | Putnam County |

| Inverness | Citrus County |

| Islamorada | Monroe County |

| Islandia | Miami-Dade County |

| Jacksonville Beach | Duval County |

| Jacksonville | Duval County |

| Jacob | Jackson County |

| Jasper | Hamilton County |

| Jay | Santa Rosa County |

| Jennings | Hamilton County |

| Juno Beach | Palm Beach County |

| Jupiter | Palm Beach County |

| Jupiter Inlet Colony | Palm Beach County |

| Jupiter Island | Martin County |

| Kenneth City | Pinellas County |

| Key Biscayne | Miami-Dade County |

| Key Colony Beach | Monroe County |

| Key West | Monroe County |

| Keystone Heights | Clay County |

| Kissimmee | Osceola County |

| La Crosse | Alachua County |

| LaBelle | Hendry County |

| Lady Lake | Lake County |

| Lake Alfred | Polk County |

| Lake Buena Vista | Orange County |

| Lake Butler | Union County |

| Lake City | Columbia County |

| Lake Clarke Shores | Palm Beach County |

| Lake Hamilton | Polk County |

| Lake Helen | Volusia County |

| Lake Mary | Seminole County |

| Lake Park | Palm Beach County |

| Lake Placid | Highlands County |

| Lake Wales | Polk County |

| Lake Worth | Palm Beach County |

| Lakeland | Polk County |

| Lantana | Palm Beach County |

| Largo | Pinellas County |

| Lauderdale Lakes | Broward County |

| Lauderdale-by-the-Sea | Broward County |

| Lauderhill | Broward County |

| Laurel Hill | Okaloosa County |

| Lawtey | Bradford County |

| Layton | Monroe County |

| Lazy Lake | Broward County |

| Lee | Madison County |

| Leesburg | Lake County |

| Lighthouse Point | Broward County |

| Live Oak | Suwannee County |

| Longboat Key | Sarasota County |

| Longboat Key | Manatee County |

| Longwood | Seminole County |

| Lynn Haven | Bay County |

| Macclenny | Baker County |

| Madeira Beach | Pinellas County |

| Madison | Madison County |

| Maitland | Orange County |

| Malabar | Brevard County |

| Malone | Jackson County |

| Manalapan | Palm Beach County |

| Mangonia Park | Palm Beach County |

| Marathon | Monroe County |

| Marco Island | Collier County |

| Margate | Broward County |

| Marianna | Jackson County |

| Marineland | St. Johns County |

| Marineland | Flagler County |

| Mary Esther | Okaloosa County |

| Mascotte | Lake County |

| Mayo | Lafayette County |

| McIntosh | Marion County |

| Medley | Miami-Dade County |

| Melbourne | Brevard County |

| Melbourne Beach | Brevard County |

| Melbourne Village | Brevard County |

| Mexico Beach | Bay County |

| Miami Beach | Miami-Dade County |

| Miami Gardens | Miami-Dade County |

| Miami Lakes | Miami-Dade County |

| Miami Shores Village | Miami-Dade County |

| Miami Springs | Miami-Dade County |

| Miami | Miami-Dade County |

| Micanopy | Alachua County |

| Midway | Gadsden County |

| Milton | Santa Rosa County |

| Minneola | Lake County |

| Miramar | Broward County |

| Monticello | Jefferson County |

| Montverde | Lake County |

| Moore Haven | Glades County |

| Mount Dora | Lake County |

| Mulberry | Polk County |

| Naples | Collier County |

| Neptune Beach | Duval County |

| New Port Richey | Pasco County |

| New Smyrna Beach | Volusia County |

| Newberry | Alachua County |

| Niceville | Okaloosa County |

| Noma | Holmes County |

| North Bay Village | Miami-Dade County |

| North Lauderdale | Broward County |

| North Miami | Miami-Dade County |

| North Miami Beach | Miami-Dade County |

| North Palm Beach | Palm Beach County |

| North Port | Sarasota County |

| North Redington Beach | Pinellas County |

| Oak Hill | Volusia County |

| Oakland | Orange County |

| Oakland Park | Broward County |

| Ocala | Marion County |

| Ocean Breeze Park | Martin County |

| Ocean Ridge | Palm Beach County |

| Ocoee | Orange County |

| Okeechobee | Okeechobee County |

| Oldsmar | Pinellas County |

| Opa-locka | Miami-Dade County |

| Orange City | Volusia County |

| Orange Park | Clay County |

| Orchid | Indian River County |

| Orlando | Orange County |

| Ormond Beach | Volusia County |

| Otter Creek | Levy County |

| Oviedo | Seminole County |

| Pahokee | Palm Beach County |

| Palatka | Putnam County |

| Palm Bay | Brevard County |

| Palm Beach | Palm Beach County |

| Palm Beach Shores | Palm Beach County |

| Palm Beach Gardens | Palm Beach County |

| Palm Coast | Flagler County |

| Palm Shores | Brevard County |

| Palm Springs | Palm Beach County |

| Palmetto | Manatee County |

| Palm Harbor | Pinellas County |

| Palmetto Bay | Miami-Dade County |

| Panama City | Bay County |

| Panama City Beach | Bay County |

| Parker | Bay County |

| Parkland | Broward County |

| Paxton | Walton County |

| Pembroke Park | Broward County |

| Pembroke Pines | Broward County |

| Penney Farms | Clay County |

| Pensacola | Escambia County |

| Perry | Taylor County |

| Pierson | Volusia County |

| Pine Crest | Miami-Dade County |

| Pinellas Park | Pinellas County |

| Plant City | Hillsborough County |

| Plantation | Broward County |

| Polk City | Polk County |

| Pomona Park | Putnam County |

| Pompano Beach | Broward County |

| Ponce De Leon | Holmes County |

| Ponce Inlet | Volusia County |

| Port Ornage | Volusia County |

| Port Richey | Pasco County |

| Port St. Lucie | St. Lucie County |

| Port St. Joe | Gulf County |

| Punta Gorda | Charlotte County |

| Quincy | Gadsden County |

| Raiford | Union County |

| Reddick | Marion County |

| Redington Beach | Pinellas County |

| Redington Shores | Pinellas County |

| Riviera Beach | Palm Beach County |

| Rockledge | Brevard County |

| Royal Palm Beach | Palm Beach County |

| Safety Harbor | Pinellas County |

| Saint Leo | Pasco County |

| San Antonio | Pasco County |

| Sanford | Seminole County |

| Sanibel | Lee County |

| Sarasota | Sarasota County |

| Satellite Beach | Brevard County |

| Sea Ranch Lakes | Broward County |

| Sebastian | Indian River County |

| Seabring | Highlands County |

| Seminole | Pinellas County |

| Sewall’s Point | Martin County |

| Shalimar | Okaloosa County |

| Sneads | Jackson County |

| Sopchoppy | Wakulla County |

| South Bay | Palm Beach County |

| South Daytona | Volusia County |

| Sounty Miami | Miami-Dade County |

| South Palm Beach | Palm Beach County |

| South Pasadena | Pinellas County |

| Southwest Ranches | Bay County |

| Springfield | Bay County |

| St. Augustine Beach | St. Johns County |

| St. Augustine | St. Johns County |

| St. Cloud | Osceola County |

| St. Lucie Village | St. Lucie County |

| St. Marks | Wakulla County |

| St. Pete Beach | Pinellas County |

| St. Petersburg | Pinellas County |

| Starke | Bradford County |

| Stuart | Martin County |

| Sun City Center | Hillsborough County |

| Sunny Hills | Washington County |

| Sunny Isles Beach | Miami-Dade County |

| Sunrise | Broward County |

| Surfside | Miami-Dade County |

| Sweetwater | Miami-Dade County |

| Tallahassee | Leon County |

| Tamarac | Broward County |

| Tampa | Hillsborough County |

| Tarpon Springs | Pinellas County |

| Tavares | Lake County |

| Temple Terrace | Hillsborough County |

| Tequesta | Palm Beach County |

| Titusville | Brevard County |

| Treasure Island | Pinellas County |

| Trenton | Gilchrist County |

| Umatilla | Lake County |

| Valpariso | Okaloosa County |

| Venice | Sarasota County |

| Vernon | Washington County |

| Vero Beach | Indian River County |

| Virginia Gardens | Miami-Dade County |

| Waldo | Alachua County |

| Wauchula | Hardee County |

| Wausau | Washington County |

| Webster | Sumter County |

| Weeki Wachee | Hernando County |

| Welaka | Putnam County |

| Wellington | Palm Beach County |

| West Melbourne | Brevard County |

| West Miami | Miami-Dade County |

| West Palm Beach | Palm Beach County |

| Weston | Broward County |

| Westville | Holmes County |

| Wewahitchka | Gulf County |

| White Springs | Hamilton County |

| Wildwood | Sumter County |

| Williston | Levy County |

| Wilton Manors | Broward County |

| Windermere | Orange County |

| Winter Garden | Orange County |

| Winter Haven | Polk County |

| Winter Park | Orange County |

| Winter Springs | Seminole County |

| Worthington Springs | Union County |

| Yankeetown | Levy County |

| Youngstown | Bay County |

| Zephyrhills | Pasco County |

| Zolfo Springs | Hardee County |