Refinance To Stop Foreclosure In Florida

A stop-foreclosure refinance is an emergency bailout refinance to stop foreclosure and. This financial strategy is usually an alternative high-interest mortgage refinancing loan option that pays off a defaulted mortgage to immediately stop the foreclosure sale. Foreclosure bailout refinancing allows Florida property owners with bad credit or missed payments, or loan modification, to refinance and buy time, preserve their equity, and stabilize their finances until they can refinance back into a low-interest loan.

Refinance Lis Pendens To Stop Foreclosure

Stop Foreclosure Refinance Situations Include:

| Divorce Buyout | ||||

| Refinance Probate | Balloon Refinance | |||

| Refinance Probate | ||||

| Partial Construction | ||||

| Garnishment | ||||

| Student Loan Default | cash-out |

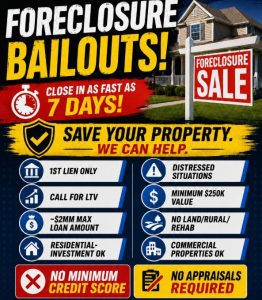

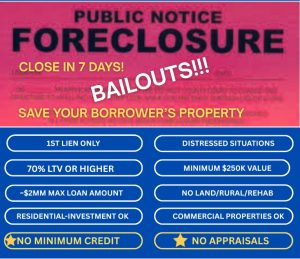

Stop Foreclosure Refinance Highlights

| Stop Foreclosure Loan Amounts • $50K to $30 million – Residential & Commercial |

Loan-to-Value (LTV) Ratios – Case By Case • Up to 70% on purchases – Up to 75% on refinance |

| Terms • 24-36 months, extension options available • Interest-only payments • Fair Rates • No prepayment penalty • Escrow may be required |

Qualification • Any Credit + All Situations Welcome • Must have equity and/or document ability to pay • Property must be in Florida • No corporate title required • Read More about Florida Bad Credit Lenders |

*All Information and terms are subject to change without notice.

Call Thomas Martin @ 954-667-9110 for the latest qualifications.

Stop Foreclosure Commerical Mortgage Refinance

Stop Foreclosure Commerical Mortgage Refinance Programs Subject To Change For Better And Worse

Commerical: Stop Foreclosure Refinance:

Refinance To Stop Foreclosure Property Types:

- Single-family home – Florida Stop Foreclosure Mortgage Lenders:

- Townhouse- Florida Stop Foreclosure Mortgage lenders:

- Duplex -Triplex- Quadplex- Stop Foreclosure Stop Foreclosure Mortgage Lenders :

- Manufactured home – Florida Stop Foreclosure Mortgage Lenders :

- Multi-Family – Florida Stop Foreclosure Mortgage Lenders:

- Modular home – Stop Foreclosure Stop Foreclosure Mortgage Lenders

- Villa – Florida Stop Foreclosure Mortgage Lenders:

- Condos- Florida Stop Foreclosure approved Condos:

- Commercial – Investment Properties:

- Condotel or Condo Hotel – Stop Foreclosure Mortgage Lenders:

- Jumbo Luxury Stop Foreclosure Mortgage Lenders:

- Co-op Florida – Stop Foreclosure Mortgage Lenders:

- Non-Warrantable Condo – Stop Foreclosure Mortgage Lenders:

- Land Lenders – Stop Foreclosure Florida Land Lenders:

- Non-Resident Stop Foreclosure Mortgage Lenders :

Stop Foreclosure Refinance Commercial:

- Bad Credit Hard Money Commerical Florida Mortgage Lenders:

- Parking lot Florida Hard Money Mortgage Lenders:

- Agricultural Hard Money Florida Mortgage Lenders:

- Car Dealership Hard Money Florida Mortgage Lenders:

- Industrial Florida Hard Money Mortgage Lenders:

- Assisted Living Home Florida Hard Money Mortgage Lenders:

- Funeral Home Florida Hard Money Mortgage Lenders:

- Multifamily Hard Money Florida Mortgage Lenders:

- HOA Mortgage Lenders In Florida:

- Vacant Land Florida Hard Money Lenders:

- Commerical Land Florida Hard Money Lenders:

- Hotel Hard Money Florida Mortgage Lenders:

- Motel Hard Money Florida Mortgage Lenders:

- Inherited Commercial Property Refinance Before Probate:

- Warehouse Florida Hard Money Mortgage Lenders:

- Stop Foreclosure Commerical Mortgage Lenders Florida:

- Finish Construction Florida Hard Money Lenders:

- Commerical Refinance Before Probate In Florida:

- Refinance Hard Money Florida Commerical Pace Loan:

- Luxury Mansion Florida Hard Money Mortgage Lenders :

- Cashout Refinace Commercial Property Listed For Sale In Florida:

- Commerical Florida Refinance Buyout Partner:

- Golf Course Florida Hard Money Mortgage Lenders:

- And More call me even if your property is not listed!

Stop Foreclosure Refinance In Florida:

- Refinance Florida HOA To Stop Foreclosure :

- Refinance Florida Lis Pendens :

- Refinance Florida Claim of lien :

- Refinance To Pay Florida Tax Lien :

- Refinance Florida Code Violations :

- Refinance Florida property Taxes :

- Refinance Florida Final Judgment :

- Buy-Out-Florida Mortgage Refinance :

- Refinance Florida Mortgage With Repossession :

- Refinance Mortgage with 30-60-90 day late payments :

- Refinance Balloon Mortgage In Florida

- Refinance Florida mortgage with collection accounts:

- Refinance To Pay Florida Property Taxes:

- Refinance (ARM) Adjustable Rate Mortgage In Florida

- Refinance Florida Department of Revenue Warrant :

- Refinance Florida Mortgage While in Bankruptcy :

- Refinance Florida Mortgage Divorce Buyout :

- Cashout Refinance While In Florida Jail:

- Stop Foreclosure Florida Mortgage Refinance:

- Refinance Florida Homeowners Association :

- Refinance Partial Construction Stop Foreclosure In Florida:

- Foreign National Stop Foreclosure Florida Mortgage Refinance:

- Florida Balloon Mortgage Refinance In Florida :

FHA Partial Claim Florida Stop Foreclosure Refinance:

An FHA partial claim is a loss mitigation option that helps borrowers behind on their Florida FHA mortgage get current. The FHA advances funds (up to 30% of the unpaid principal balance) as an interest-free, subordinate loan to cover missed payments. You don’t have to make monthly payments on it, and it must be repaid when you sell, refinance, or pay off the primary mortgage.

Benefits of an FHA Partial Claim Mortgage Refinance

Zero-interest loan: The FHA Partial Claim loan is a deferred balance that does not accrue interest, meaning the amount you owe will never increase.

No Monthly Payments: You will resume your normal, on-time mortgage payments, and the partial claim remains completely deferred.

Payment Supplement: The FHA partial claim loan includes a Payment Supplement option, which allows a partial claim to provide a temporary 3-year reduction in your monthly mortgage payment.

Repayment Triggers: Repayment of the lien is only required if you sell the home, transfer the title, pay off the primary mortgage, or refinance.

FHA Partial Claim Loan Eligibility

To qualify for an FHA partial claim refinance, you generally must meet the following criteria:

FHA-Backed Loan: Your current mortgage must be insured by FHA.

Financial Hardship: You must have experienced a verifiable financial hardship that caused you to fall behind on payments (usually by at least 61 days). And, you now must document the ability to repay.

Ability to Pay: You must demonstrate that you have overcome the hardship and can resume your regular monthly mortgage payments.

Owner-Occupied: The property must be your primary residence

How To Check Your Foreclosure Auction Status in Florida:

- Get the case info: Find your foreclosure case number in the county records search or the trustee’s name from the Notice of Default/Notice of Trustee Sale, mortgage statement, or Florida mortgage lender correspondence. If you don’t have them, look up the property address on the Florida county clerk’s public records to find foreclosure filings.

- Check the county Clerk of Court docket: Search the county clerk’s online civil docket by case number or party name to view filings, hearing dates, motions, and orders. This shows the current status (scheduled sale, continued, stayed, or final judgment).

- Look up the trustee sale listing/auction portal: Many Florida counties list trustee/tax‑deed sales on online auction platforms (e.g., RealAuction, Bid4Assets) or trustee websites. Search by property address or case number to see scheduled sale dates and auction status.

- Review the Florida Foreclosure Notice of Sale ads: The Notice of Sale is published in the county legal newspaper before auction. Check local legal notices or the county’s legal‑notices portal to confirm the advertised sale date and any continuances.

- Contact the trustee or the lawyer’s firm handling the sale: Florida foreclosure counsel contact info is on the Notice of Sale. Call/email to confirm whether the sale is still scheduled, has been continued, or canceled.

- Confirm sheriff/auction procedures & timing: Some counties hold sales at courthouse steps; others use online auctions. Verify exact sale time, platform, and bidder registration requirements.

- Check for bankruptcy filings & lis pendens: Search the bankruptcy docket (PACER or the county’s bankruptcy clerk) and the clerk’s records for a filed lis pendens or bankruptcy stay that would halt the sale.

- Tax & title checks: Use the county property appraiser and tax collector sites to confirm owner name, parcel/APN, and any tax delinquencies or certificates that may affect the sale outcome.

- Contact the lender/servicer or hire counsel/title company: If you’re the owner and need to stop a sale, contact the servicer immediately about reinstatement, payoff, loan modification, or loss mitigation. For purchasers/agents, use a title company to confirm curative actions.

- Document everything & act fast: Foreclosure timelines move quickly. Keep copies of notices, emails, and proof of payment/negotiation attempts. If you need to stop a sale, act immediately – often hours or days before the auction.

Options to Stop Foreclosure in Florida

- Foreclosure Refinance (Hard Money Loans): If you are facing foreclosure in Florida but have significant equity, private hard-money Florida lenders specialize in creative real estate mortgage options to pay off your arrears. These Florida hard money loans require more equity, non-owner occupancy, or a solid exit strategy.

- Loan Modification: The most common first step to stop foreclosure in Florida is to negotiate directly with your current mortgage lender to modify your loan terms, which may include stacking the arrears on the back of the loan, lowering the interest rate, or extending the term.

- Chapter 13 Bankruptcy: Filing for Florida bankruptcy immediately triggers an “automatic stay,” stopping the foreclosure, giving you a court-approved 3-to-5-year repayment plan to catch up on missed mortgage payments.

- Deed-in-Lieu or Short Sale: If keeping the property is no longer an option, you can voluntarily give the property back to the bank (Deed-in-Lieu) or sell it for less than what is owed (Short Sale) to mitigate credit damage.

Foreclosure Bailout Refinance For Business Purposes and Non-owner-occupied Only

The undersigned understands that, because these loans are for business purposes, the Loan may not be subject to

the requirements of certain federal and Florida state consumer protection, mortgage lending, or other laws, including but not limited to the provisions of the federal Truth-in-Lending Act (15 U.S.C. §§ 1601 et seq.) and its implementing

Regulation Z (12 C.F.R. Part 1026), Real Estate Settlement Procedures Act (12 U.S.C. § 2601 et seq.) Exempt from Ability to Repay and Qualified Mortgage Standards Under the Truth in Lending Act (Regulation Z), Gramm-Leach-Bliley Act (15 U.S.C.§§ 6802-6809), Secure and Fair Enforcement Mortgage Licensing Act (12 U.S.C. § 5101 et seq.),

and Homeowners Protection Act (12 U.S.C. § 4901 et seq.), and that my ability to avail myself of the protections offered under federal and state laws for consumer purposes, residential mortgage loans may be limited.

Top Reasons People Need A Foreclosure Bailout In Florida

Stop Foreclosure Refinance For Unforeseen Income & Employment Shocks

- Job loss, reduced hours, or business failure

- Sudden loss of primary income earner (death, disability)

- Seasonal or gig income shortfalls for self‑employed Florida homeowners.

Stop Foreclosure, Cashout Refinance to Pay Medical & family emergencies

- Major medical expenses or long‑term care costs

- Emergency family needs (care for ill relative, unexpected childcare costs)

- Cash-out Refinance To Pay Medical Bills and Medical Collection Accounts.

- Funeral and estate expenses after a death

Stop Foreclosure Refinance For Debt Consolidation & Cash-flow Problems

- Excessive credit‑card or unsecured debt → unaffordable payments

- Aggressive collection actions, judgments, or wage garnishments

- Balloon loan or ARM reset causing payment spike

- HELOC demand or maturity requiring payoff

Stop Foreclosure Refinance For: Taxes, liens & assessments

- Delinquent property taxes risk tax deed sale

- IRS or state tax liens creating priority encumbrances

- HOA/condo special assessments or unpaid association dues leading to association foreclosure risk

Stop Foreclosure Refinance For: Legal & court: Divorce Or Other obligations

- Stop Foreclosure Refinance to pay Large legal bills, settlements, or judgments (civil suits, divorce, child support)

- Bankruptcy plan shortfalls or need to fund a Chapter 13 plan confirmation

- Stop Foreclosure refinance to avoid chapter 7 or chapter 13 bankruptcy.

- Probation/restitution orders or criminal legal costs

Stop Foreclosure Refinance For: Title, probate & ownership issues

- Owner’s death with probate delays preventing payment or transfer of funds

- Stop Foreclosure Refinance before probate in Florida.

- Missing heirs or estate disputes are causing a payment lapse

- Title clouds or lis pendens requiring funds to clear liens

Stop Foreclosure Refinance for Property condition & insurance

- Hurricane/flood/other storm damage with delayed insurance proceeds

- Insurance cancellation or denial leading to escrow shortfall

- Urgent repair needs (roof, HVAC, structural) threatening habitability and lender demands

Stop Foreclosure Refinance in Florida: Mortgage Balloons, Adjustable Rates Or Other Issues

- Servicer errors or misapplied payments create an apparent default

- Escrow shortages (taxes/insurance) are increasing the required monthly payment

- Miscommunication or delay in the loan modification process is prompting emergency funding

Stop Foreclosure Refinance in Florida: Lifestyle & personal choices

- Divorce or partner separation requiring buyout of spouse’s equity

- Relocation costs or moving deadlines that force liquidity needs

- Addiction or financial mismanagement leading to missed payments

Stop Foreclosure Refinance in Florida : Fraud, theft & identity issues

- Identity theft resulting in fraudulent charges or redirected refunds

- Mortgage rescue/foreclosure‑relief scams that drain borrower funds

Stop Foreclosure Refinance For: Investor & rental property issues

- Tenant nonpayment or eviction costs reduce rental income

- Vacant investment property carrying costs and accelerated lender action

- Contractor liens from rehab work unpaid during flips

Stop Foreclosure Refinance in Florida: Strategic & tactical reasons

- Short bridge to sell the property (avoid foreclosure to preserve credit and resale value)

- Payoff to qualify for a refinance or to remove a problematic lien before sale

- Temporary bailout pending permanent loan modification or restructuring

Stop Foreclosure Refinance in Florida: Regulatory & municipal actions

- Code‑enforcement fines, municipal liens, or condemnation orders demanding immediate cure

- Special assessments (stormwater, sidewalk, local improvement) are unexpectedly billed

Stop Foreclosure Refinance in Florida For: Other unexpected shocks

- Large, unexpected household expenses (education, sudden travel for a family crisis)

- Loss of co‑borrower income (business partner withdraws support)

- Rapid interest‑rate environment changes, raising variable payments elsewhere that cascade into mortgage distress

Refinance Florida Business Loans Only To Stop Foreclosure

You can pledge a Florida homestead home as collateral for a mortgage loan in Florida, but it’s risky. Refinancing a business‑purpose loan secured by a homestead will void protections, trigger creditor claims, or lead to loss of the homestead exemption. Here is a concise list of business-loan Florida refinance purposes options

Common Florida Business Purpose Refinancing Reasons

- Working business capital in Florida Business Refinance covers day‑to‑day expenses, payroll, and shortfalls.

- Equipment purchase, Florida Business Refinance, buy or lease machinery, vehicles, or tech.

- Inventory financing for Florida Business Refinance purchase seasonal or bulk inventory.

- Real estate acquisition in Florida, Business Refinance, buy owner‑occupied or investment property.

- Construction/tenant build‑out, Florida Business Refinance fund build, renovation, or leasehold improvements.

- Business acquisition, Florida Business Refinance, buy another business, or buy out a partner.

- Debt refinance / consolidation, Florida Business Refinance, pay off high‑interest loans or credit lines.

- Bridge financing for Florida Business Refinance short‑term gap until permanent financing or sale.

- SBA loan (7a/504) uses Florida Business Refinance for long‑term real estate or equipment purchase with SBA guarantees.

- Franchise financing, Florida Business Refinance, purchase franchise rights, and initial setup.

- Purchase‑order / receivables financing Florida Business Refinance fund production against confirmed orders or AR.

- Expansion / new location, Florida Business Refinance, open an additional store/office or enter a new market.

- Seasonal financing Florida Business Refinance cover peaks in payroll/inventory for seasonality.

- Emergency/disaster recovery, Florida Business Refinance, repair or replace assets after damage.

- Technology/software investment, Florida Business Refinance, buy or develop IT systems, ERP, or e‑commerce platforms.

- Marketing/growth capital, Florida Business Refinance fund, customer acquisition, rebranding, or product launches.

- Legal / settlement funding, Florida Business Refinance, pay litigation/legal fees, or settlement requirements.

- Employee hiring & training, Florida Business Refinance scale staff for growth initiatives.

Refinance Business Purpose Examples

- Refinance For Working business capital to cover payroll and vendor payments during the seasonal slowdown.

- Refinance a Florida balloon mortgage that’s due.

- Refinance a Florida adjustable-rate mortgage that’s due.

- Refinance XYZ manufacturing equipment to increase capacity by 40%.

- Refinance commercial Florida property at 123 Main St for owner‑occupied HQ.

- Refinance existing high‑interest lines to reduce monthly debt service.

- Bridge loan to complete renovation and stabilize rental income before long‑term refinancing.

- Refinance SBA 7(a) loan to acquire competitor and integrate operations.

- Refinance the inventory loan to purchase holiday stock for increased Q4 demand.

- Refinance to fund production against a confirmed $250k order with a major retailer.

- Refinance tenant buildout for new retail location and related soft costs.

- Refinance to buy an existing franchise and cover initial working capital.

CASHOUT REFINACE BUSINESS DISCLOSURE, CERTIFICATION, AND ACKNOWLEDGEMENT FOR BUSINESS PURPOSE LOANS ONLY

Borrower/Guarantor Certification You hereby warrant and represent that you wish to continue with the business loan refinance application, that the loan is for Florida business purposes and not consumer purposes, and that the loan proceeds are intended to be used and shall be used for Florida business purposes only, not for personal, family, or household purposes. You also represent that none of the properties securing the loan is currently occupied by you of your family as a primary residence or vacation home, but instead all properties are leased or intended to be leased or occupied by an entity or person other than you or your family, and that during the term of the loan you shall not occupy or reside in any of the properties for more than fourteen (14) days in any calendar year.

Cashout Refinance Stop Foreclosure Florida Business Loan Disclosures

Because the Florida business loan will be made exclusively for business purposes, certain federal laws applicable to consumer-purpose loans will not apply to this loan. Among federal laws that are not applicable to a business loan are the Truth in Lending Act (15 U.S.C. § 1601 et seq.) Real Estate Settlement Procedures Act (12 U.S.C. § 2601 et seq.), Secure and Fair Enforcement Mortgage Licensing Act (12 U.S.C. § 5101 et seq.), and Homeowners Protection Act (12 U.S.C. § 4901 et seq.). A number of rights, including the following rights, which would apply if the loan were a consumer purpose loan, will not apply to you because the loan for which you applied is a business purpose loan:

Refinance Property Taxes To Stop Foreclosure

Florida Tax Liens: Florida Tax liens are the primary liens that can lead to a foreclosure sale. Local (county or city) l governments can place a lien for unpaid Florida property taxes. These are significant because they often hold priority over all other Florida liens, including the primary property’s mortgage.

Stop Foreclosure With an Asset-Based Lender

Our commerical Florida mortgage lenders have options to stop foreclosure on commercial properties through “foreclosure buyout” loans and bridge financing, targeting small-balance Florida commercial and investment properties. As a private Florida Stop Foreclosure mortgage lender, they offer quick-closing, asset-based loans (often ignoring credit scores or personal income) to bail out Florida commerical property owners facing bank foreclosure.

Stop Foreclosure Sale Leaseback In Florida

The sale-leaseback program is great for people who cannot hold onto their Florida investment property for some reason. We will use the remaining investment money to bring the property up to working condition and at least back to 12-60 months, allowing you to purchase it back once you have your financing in order.

- We will buy your property and pay off all debts

- We will lease it back to you for a reasonable monthly payment that you can afford

- You can buy it back from us for a set price that we both agree on anytime for up to 5 years

- Ability to deal with performing as well as non-performing assets

- A great option to retain your property that might otherwise be in jeopardy

- If the property needs work, we will even advance the money to fix it up

- We can move FAST and CLOSE QUICKLY

- All Florida property types except land

Commerical Stop Foreclosure Refinance

- No Income Verification: Commerical Foreclosure Loans are based primarily on the property’s value, not the borrower’s personal credit or income, often closing in as few as 10 days.

- No Credit Requirements: credit Score or payment history not considered.

- Foreclosure Refinance / Bailouts: They provide loans to pay off lenders who are initiating foreclosures, aimed at saving commercial, mixed-use, and investment properties.

- Short-term Funding: These foreclosure loan options provide short-term (typically 24-36 months) financing to cover immediate needs such as debt repayment, inventory purchases, or real estate transactions while the borrower secures long-term funding. They are designed to “bridge the gap” between a current obligation and future, more permanent financing.

- Targeted Properties: Focus on small-balance commercial, non-owner-occupied properties, and investment real estate.

Refinancing to Stop Foreclosure In Florida

- Requirements: You generally need significant property equity to qualify for a new loan that pays off the current lender, including missed payments and the attorney foreclosure fees.

- Short Refinance: If you owe more than your home is worth, your Florida mortgage lender might consider a “short refinance,” where you receive a new loan for a lower amount than your outstanding balance.

Yes, you can cash-out refinance while in a Florida Jail for residential, commercial, and land for non-owner-occupied property – NON Florida Homestead property types while in jail. Our Bad credit Florida Jail mortgage lenders can help cashout refinancing balloon mortgages, Collection accounts, judgments, adjustable rates, liens, property taxes, judgments, Lis pendens, Claims of lien, Florida Jail tax liens, Bankruptcy, Code violations, Final judgments, Buyouts, Late payments, Tax lien, Department of Revenue, Behind On HOA, Stop-Foreclosure, Probate, Divorce, or Partner buyouts.

Alternatives to Stop Foreclosure In Florida:

- Loan Modification: The lender changes the original loan terms to make payments more affordable (e.g., a lower interest rate or a longer term).

- Reinstatement: Paying the total past-due amount plus fees in a lump sum.

- Forbearance: Temporarily pausing or reducing payments if the hardship is short-term.

- Chapter 13 Bankruptcy: Filing for bankruptcy triggers an “automatic stay,” which halts foreclosure and allows you to repay missed payments over 3–5 years.

- All legal alternatives should be discussed with your attorney.

Stop Foreclosure In Florida Action Steps:

- Contact Your Mortgage Servicer: Call them immediately to discuss repayment options and stop foreclosure.

- Get Free Counseling: Contact a HUD-approved housing counselor to explore options at no cost.

- State Local Programs: Check for county, State, and local nonprofit stop-foreclosure programs.

- Contact Family: Contact your family to cosign or help restate your mortgage to Stop Foreclosure.

- Raise Money: Start a GoFundMe or ask the community to help you stop foreclosure.

- Gather Documents: Prepare your financial records (income, tax returns).

- Avoid Scams: Be wary of companies promising to stop foreclosure for large upfront fees.

- Sell Your Property: If you have equity, use it and move on.

Cashout Refinance HOA To Stop Foreclosure

Yes, you can cash-out refinance to pay your past-due HOA payments and stop foreclosure in Florida. If you are past due on the Florida Homeowners Association (HOA), the HOA has most likely filed a Florida lis pendens on your Florida property to recover the delinquent payments. A Florida lis pendens signifies a legal action against your Florida property related to unpaid HOA fees and or other Florida violations. A Florida lis pendens creates a cloud on the title, making it difficult to sell or refinance your Florida property until the association files a RELEASE OF LIS PENDENS. Under the right circumstances, you may be able to refinance past-due HOA payments. The Florida HOA is likely pursuing legal action to recover the unpaid fees and might be in the process of foreclosure.

Cash Out Refinance Before Probate

Yes, Cashout Refinance Residential & Commercial Florida Property Refinance In Probate – With No Minimum Credit Score. Cash-out refinancing an inherited Florida property in probate offers several key benefits, primarily allowing an heir to secure cash-out of the equity for various purposes. To accomplish this, a private estate Florida mortgage lender will place a lien on the estate until the probate process is complete. Refinancing a Florida buyout of an inherited home enables you to pay off any existing liens and cash out to buy out any family members’ ownership interest, or Stop Foreclosure, even pay off collection accounts. Inheritance cash-out refinancing simplifies the process of buying out family members in exchange for sole ownership of the property, while providing the necessary resources to execute a successful buyout.

120-Day: Stop Foreclosure In Florida Rule

Under the CFPB’s Stop Foreclosure Mortgage Servicing Rules, Florida mortgage servicers generally cannot start the formal Florida foreclosure process until a borrower is more than 120 days delinquent. This 120-day period is designed to give homeowners time to explore loss mitigation options (alternatives to stop foreclosure in Florida and avoid losing their home.

Stop Foreclosure In Florida Considerations:

Exceptions: Foreclosure can begin before 120 days if the borrower has abandoned the property, has not responded to outreach, or has exhausted all other options. This may not apply to private lenders.

Loss Mitigation: If a complete loss mitigation application is received before the 120-day period expires, the foreclosure cannot proceed until the application is reviewed.

Small Servicers: A “small servicer”Florida Business Refinance one that services 5,000 or fewer mortgages, which they also ownFlorida Business Refinance is exempt from some of these rules.

Timeline: The 120-day period typically begins after the first missed payment. The servicer cannot file the first legal notice of foreclosure during this time.

Purpose: The rule allows borrowers to work with Florida mortgage lenders on loan modifications, short sales, or other solutions to stop foreclosure.

If you are facing foreclosure, you should contact your servicer or a HUD-approved Florida housing counselor.

Steps To Stop Foreclosure In Florida

- Call your current lender and work out a repayment plan.

- Call the county, state, and city, and search for stop foreclosure programs in your area.

- Reach this hotline by dialing 1-888-995-HOPE. You may also obtain a list of U.S. Department of Housing and Urban Development (HUD)- certified stop foreclosure Florida counselors by clicking here.

Refinance Florida Commercial Stop Foreclosure

Multifamily Stop Foreclosure mortgage refinancing (5+ Units):

Florida multifamily Stop Foreclosure mortgage refinancing for apartment investors, operators, and developers across Austin, Dallas-Fort Worth, Houston, and San Antonio. Florida Stop Foreclosure offers mortgage refinancing structures and competitive capital for stabilized and value-add apartment communities throughout Florida.

Industrial & Warehouse Stop Foreclosure mortgage refinance:

Florida industrial and warehouse Stop Foreclosure mortgage refinancing for distribution centers, flex space, logistics facilities, and owner-occupied industrial properties. With continued population growth, Florida remains one of the strongest industrial real estate markets in the country. Stop Foreclosure mortgage refinancing structures competitive debt solutions for investors, developers, and business owners seeking capital for stabilized, value-add, or development industrial assets.

Hotel & Hospitality Stop Foreclosure mortgage refinancing

Florida hotel and hospitality Stop Foreclosure mortgage refinancing for flagged and independent properties across Florida, including Miami, Palm Beach, Fort Lauderdale, Hollywood, Jacksonville, Tampa, Orlando, Port St Lucie, Pembroke Pines, Miramar, Cape Coral, St Petersburg, Palm Bay, Gainesville, Coral Springs, Lakeland, Springhill, Pompano beach, Brandon, Miami, CLearwater, Riverview, Tampa, Palm Coast Davie, Fort Myers, Naples.and all Florida. From select-service acquisitions to full-service repositioning and new construction developments, Florida Stop Foreclosure offers mortgage refinancing structures and capital solutions aligned with occupancy performance, brand affiliation, and market demand across Florida.

Office & Retail Property Stop Foreclosure mortgage refinancing

Florida office and retail Stop Foreclosure mortgage refinancing solutions for stabilized, value-add, and owner-occupied commercial properties across Florida, Fort Lauderdale, Hollywood, Jacksonville, Tampa, Orlando, Port St Lucie, Pembroke Pines, Miramar, Cape Coral, St Petersburg, Palm Bay, Gainesville, Coral Springs, Lakeland, Springhill, Pompano beach, Brandon, Miami, CLearwater, Riverview, Tampa, and growing secondary markets. Florida Stop Foreclosure mortgage refinancing structures capital for neighborhood retail centers, medical office buildings, corporate office assets, and mixed-use properties throughout Florida. We align each transaction with current lender appetite, tenant stability, and market fundamentals.

Ground-Up Construction Stop Foreclosure mortgage refinancing:

Florida commercial construction Stop Foreclosure mortgage refinancing for developers and sponsors building multifamily, industrial, retail, hospitality, and mixed-use projects across Austin, Dallas-Fort Worth, Houston, San Antonio, and high-growth secondary markets.

Florida Stop Foreclosure mortgage refinancing includes:

structures, construction capital solutions aligned with project feasibility, sponsor experience, and Florida market demand. From entitlement through stabilization, we coordinate Stop Foreclosure mortgage refinancing that supports disciplined execution and long-term investment performance.

Relevant Terms: To Stop Foreclosure

If you are working with your mortgage servicer or an approved Florida housing counselor to keep your home, there are several options:

- Repayment Plan: This is an agreement that gives you a fixed amount of time to repay the amount you are behind by combining a portion of what is past due with your regular monthly payment. At the end of the repayment period, you have gradually paid back the delinquent amount of your mortgage.

- Loan Modification: A written agreement between you and your mortgage servicer that permanently changes one or more of the original terms of your note to make your payments more affordable.

- Reinstatement: Your servicer may agree to let you pay the total amount you are behind, in a lump sum payment and by a specific date. This is often combined with forbearance when you can show that funds from a bonus, tax refund or other source will become available at a specific time in the future. Be aware that reinstatement plans may incur late fees and other costs.

- Forbearance: Your servicer may offer a temporary reduction or suspension of your mortgage payments while you get back on your feet. Forbearance is often combined with a reinstatement or a repayment plan to catch up on missed or reduced mortgage payments. Please be aware that some forbearance plans require you to immediately repay the missed payments in a lump sum at the end of the plan.

If you and your Florida mortgage servicer agree that you cannot keep your home, there may still be options to avoid foreclosure:

- Stop Foreclosure Refinancing: While refinancing is not necessarily a good option when facing foreclosure and can sometimes be predatory, there are instances where it may help. Talk to your servicer to see if refinancing is an option for you.

- Short Payoff: If you can sell your house, but the sale proceeds are less than the total amount you owe on your mortgage, your mortgage servicer may agree to a short payoff and write off the portion of your mortgage that exceeds the net proceeds from the sale.

- Deed-in-Lieu of Foreclosure: A deed-in-lieu of foreclosure is a cancellation of your mortgage if you voluntarily transfer title of your property to your mortgage servicer. Usually, you must try to sell your home for its fair market value for at least 90 days before a mortgage company will consider this option. A deed-in-lieu of foreclosure may not be an option if there are other liens on the property, such as second mortgages, judgments from creditors or tax liens.

- Assumption: An assumption permits a qualified buyer to take over your mortgage debt and make the mortgage payments, even if the mortgage is non-assumable. As a result, you may be able to sell your property and avoid foreclosure.

Florida Stop Foreclosure “Rescue” Scams

Contact your Florida mortgage loan servicer as soon as you realize you have missed a payment.

Florida Mortgage Servicers can discuss options with you to help you work through payments during difficult financial times. Servicers prefer to keep you in your Florida home, and most will work with you to find a solution if you can prove your ability to repay. Be honest with your servicer about your financial hardship so that you can have a realistic discussion regarding your options. You can find the number for your monthly mortgage statement.

Understand your rights.

Learn all that you can about your mortgage rights and foreclosure laws in Florida. Review your loan documents to determine what your Florida mortgage lender or servicer may do if you can’t make your payments. Review Florida laws, particularly Florida Statutes Chapter 702, to learn about foreclosure proceedings.

Understand the relevant terms.

If you are working with your Florida mortgage servicer to Stop foreclosure to keep your Florida home, there are several options:

- Repayment Plan: This is an agreement that gives you a fixed amount of time to repay the amount you are behind by combining a portion of what is past due with your regular monthly payment. At the end of the repayment period, you have gradually paid back the amount of your Florida mortgage that was delinquent.

- Loan Modification: A written agreement between you and your mortgage servicer that permanently changes one or more of the original terms of your note to make your payments more affordable.

- Reinstatement: Your servicer may agree to let you pay the total amount you are behind, in a lump sum payment and by a specific date. This is often combined with forbearance when you can show that funds from a bonus, tax refund or other source will become available at a specific time in the future. Be aware that there may be late fees and other costs associated with a reinstatement plan.

- Forbearance: Your servicer may offer a temporary reduction or suspension of your mortgage payments while you get back on your feet. Forbearance is often combined with a reinstatement or a repayment plan to pay off the missed or reduced mortgage payments. Please be aware that some forbearance plans require that you immediately pay back the missed payments in a lump sum at the end of the plan.

If you and your servicer agree that you cannot keep your Florida home, there may still be options to stop foreclosure:

- Short Payoff: If you can sell your Florida house but the sale proceeds are less than the total amount you owe on your mortgage, your mortgage servicer may agree to a short payoff and write off the portion of your mortgage that exceeds the net proceeds from the sale.

- Deed-in-Lieu of Foreclosure: A deed-in-lieu of foreclosure is a cancellation of your mortgage if you voluntarily transfer title of your property to your mortgage servicer. Usually you must try to sell your home for its fair market value for at least 90 days before a mortgage company will consider this option. A deed-in-lieu of foreclosure may not be an option if there are other liens on the property, such as second mortgages, judgments from creditors or tax liens.

- Assumption: An assumption permits a qualified buyer to take over your mortgage debt and make the mortgage payments, even if the mortgage is non-assumable. As a result, you may be able to sell your property and avoid foreclosure.

- Stop Foreclosure Refinancing: While refinancing is NOT necessarily a good option when facing foreclosure and can sometimes be predatory, there are instances where it may help. Talk to a hard money Florida mortgage lender to explore your options.

Stop Foreclosure Florida Mortgage Refinance

REFINANCE NOTICE OF DEFAULT AND FORECLOSURE SALE

WHEREAS, on a certain Jacksonville, Florida Mortgage Deed of Trust was executed by A SINGLE WOMAN AND A SINGLE MAN, AS JOINT TENANTS WITH A FULL RIGHT OF SURVIVORSHIP as trustor in favor of URBAN FINANCIAL GROUP as beneficiary, and was recorded on , as Instrument No. , in the Office of the Recorder of Jacksonville, Florida County, Florida; and

WHEREAS, the Mortgage Deed of Trust was insured by the Jacksonville, Florida United States Secretary of Housing and Urban Development (the Secretary), pursuant to the National Housing Act, for the purpose of providing

single family house; and WHEREAS, the beneficial interest in the Jacksonville, Florida Mortgage Deed of Trust is now owned by the Secretary, pursuant to an assignment dated 11/12/2018, recorded on 11/26/2018, as instrument number 115463678, in the office of Broward County, Florida; and WHEREAS, a default has been made in the covenants and conditions of the Mortgage Deed of Trust in that the payment due upon the death of the borrower(s) was not made and remains wholly unpaid as of the date of this notice, and no payment has been made sufficient to restore the loan to currency; and

WHEREAS, the entire amount delinquent as of 1/21/2026 is $288,140.71; and WHEREAS, by virtue of this default, the Secretary has declared the entire amount of the indebtedness secured by the Mortgage Deed of Trust to be immediately due and payable; NOW THEREFORE, pursuant to powers vested in me by the Single Family Mortgage Foreclosure Act of 1994, 12 U.S.C. 3751 et seq., by 24 CFR part 27, subpart B, and by the Secretary’s designation of me as

Foreclosure Commissioner, SEE ATTACHED notice is hereby given that on 3/9/2026 at 11:00 AM local time, all real and personal property at or used in connection with the following described premises (“Property”) will be sold at public auction to the highest bidder:

Stop Foreclosure Refinance Florida Lis Pendens –

You are notified of the institution of this action by Plaintiff against you seeking to foreclose a lien recorded in Broward County, Florida on the following property: TO DEFENDANTS, JOHN DOE and JANE DOE, AND ALL OTHERS WHOM IT MAY CONCERN: To the above Defendants, if they be living; and, if they be dead, the unknown Defendants who may be spouses, heirs, devisees successors or assigns of such Defendants, and additional unknown Defendants as successors in interest, grantees, assignees, lienors, creditors, trustees and all parties claiming interest by, through, under or against the Defendants who are not natural persons, who are not known to be dead or alive and all parties having or claiming to have any right, title or interest in the property described in the lien being foreclosed herein. YOU ARE NOTIFIED of the institution of this above-styled action by the named Plaintiffs against you seeking to foreclose a Claim of Lien in Miami Florida which was recorded on April 1, 2025, under Instrument #120136720 in the Public Records of Broward County, Florida: THE NATURE OF THIS ACTION IS A COMPLAINT TO FORECLOSE A CLAIM OF LIEN

FOR ASSESSMENTS.

Refinance To Stop Florida Foreclosure

LAKE HOMEOWNERS ASSOCIATION, INC., a Florida non-profit corporation, Plaintiff, V., and any and all unknown parties claiming by, through, under and against the herein named individual defendants who are now known to be dead or alive, whether said unknown parties may claim an interest as spouses, heirs, grantces, or other claimants, Defendants in Miami Florida AND ALL OTHERS WHOM IT MAY CONCERN YOU ARE NOTIFIED OF THE FOLLOWING: (a) The Plaintiff has instituted this action against you seeking to foreclose a lien, with respect to the property described below. (b) The Plaintiff in this action is: INC. HOMEOWNERS ASSOCIATION, (c) The case number of the action is as shown on the caption. (d) The property that is the subject matter of this action is in Miami-Dade County, Florida, and is described as follows: as dated 6/41/2025, SEE ATTACHED EXHIBIT “A” DEERFIELD BEACH, FL 33442 Parcel ID No.:

Refinance To Stop HOA Foreclosure In Florida

To the above Defendants, if they be living; and, if they be dead, the unknown Defendants who may

be spouses, heirs, devisees successors or assigns of such Defendants, and additional unknown Defendants

as successors in interest, grantees, assignees, lienors, creditors, trustees and all parties claiming interest

by, through, under or against the Defendants who are not natural persons, who are not known to be dead

or alive and all parties having or claiming to have any right, title or interest in the property described in

the lien being foreclosed herein. YOU ARE NOTIFIED of the institution of this above-styled action by the named Plaintiffs against you seeking to foreclose a Claim of Lien which was recorded on April , 2025, under Instrument

#5120151925375 in the Public Records of Broward County, Florida: SEE EXHIBIT “А” Pembroke Pines, FL 33025

THE NATURE OF THIS ACTION IS A COMPLAINT TO FORECLOSE A CLAIM OF LIEN FOR ASSESSMENTS.

Dated this June 151, 2025

Stop Foreclosure Fast Refinance Florida

The quickest way To Stop Foreclosure In Tampa, Florida, is to contact your Florida mortgage lender as soon as you fall behind and start a repayment plan. Tampa, Florida hard money Mortgage Lenders‘ number one goal is to stop foreclosure. Florida mortgage servicers can discuss options with you to help you work out repayment plans during difficult, tough financial times. Florida mortgage lenders prefer to have you keep your home so they can keep your mortgage in service. Be straightforward with your Florida mortgage lender about your financial circumstances so that you can have a realistic discussion regarding your options. You can find the Florida mortgage lenders’ phone number on your monthly mortgage statement or coupon book.

Potential solutions to Stop Foreclosure in Florida:

-

Loan Modification: Contact your Florida mortgage lender to discuss modifying your loan terms, such as lowering the interest rate or extending the loan term, to make payments more manageable.

-

Reinstatement: If possible, pay off the full amount of overdue payments, fees, and costs to reinstate your Florida mortgage loan and stop the foreclosure process.

-

Redemption: To Stop The foreclosure sale, you can redeem your property by paying the full outstanding mortgage balance, including all associated fees, before the sale

-

Bankruptcy: Filing for Chapter 7 or Chapter 13 bankruptcy can provide an automatic stay, temporarily halting the foreclosure process while you work on a repayment plan or other solutions. Talk to your attorney to find out if this is an option for you. I am not an attorney and i cannot give you legal advice.

-

Deed in Lieu of Foreclosure: Voluntarily transferring ownership of your property to your Florida mortgage lender can avoid the negative impact of a foreclosure sale on your credit report.

-

Mediation: In Florida, homeowners may have the option to mediate with their lender before foreclosure proceedings begin.

-

Challenging the Foreclosure: If the Florida foreclosure process was not handled correctly, you may be able to challenge it in court.

Is it legal in Florida to refinance and prepay 12 or 24 months of payments to avoid Foreclosure?

Yes, but refinancing a primary residence during a Florida foreclosure requires navigating strict judicial foreclosure timelines and federal mortgage servicing regulations. Florida homeowners must generally rely on private or subprime mortgage lenders that accept lower credit scores and alternative income verification, provided there is sufficient home equity. If a Florida homeowner is currently in foreclosure and provides an interest reserve, but refinancing primary homes in foreclosure is heavily regulated under the Florida Foreclosure Rescue Fraud Prevention Act (FFRFPA) and federal consumer finance laws. Structuring a loan to refinance a foreclosure correctly is critical to avoid its classification as an illegal predatory rescue.

What is an interest reserve is?

A portion of the loan proceeds is set aside at closing to pay interest (and sometimes PITI/escrow items) for a fixed period. The Florida mortgage lender pays the borrower’s mortgage interest from that reserve, thereby bringing payments to the original lender current.

How an interest reserve can help you stop foreclosure in Florida:

- The reserve cures arrears and reinstates the loan or prevents a sale by funding the missed payments before the foreclosure sale date.

- It can also fund short periods while a longer remedy is arranged (sale, full refinance, loan modification, bankruptcy).

Tips To Stop Foreclosure In Florida

Are you having trouble keeping up with your mortgage payments in Florida? Have you received a notice from your lender asking you to contact them?

- Don’t ignore the letters from your lender

- Contact your Florida lender immediately to stop foreclosure quickly.

If you are unable to make your monthly mortgage payment, don’t ignore the problem. Work with your mortgage lender directly until you can get back on track. If you can prove your ability to make the payments, you likely have repayment options.

1. Don’t ignore your Florida Mortgage Lender.

The further behind you become, the harder it will be to reinstate or modify your mortgage and the more likely that you will lose your house.

2. Contact your Florida mortgage lender as soon as you realize that you have a problem.

Florida mortgage lenders DO NOT want your house. They have options to help borrowers through difficult financial times.

3. Open and respond to all mail from your Florida mortgage lender.

The first notices you receive will offer good information about foreclosure prevention options that can help you weather financial problems. Later mail may include important notices of pending legal action. Your failure to open the mail will not be an excuse in foreclosure court.

4. Know your mortgage rights.

Find your loan documents and read them so you know what your lender may do if you can’t make your payments. Learn about the foreclosure laws and timeframes in your state (as every state is different) by contacting the State Government Housing Office.

5. Understand foreclosure prevention options.

Valuable information about foreclosure prevention (also called loss mitigation) options can be found online.

6. Contact a HUD-approved housing counselor.

The U.S. Department of Housing and Urban Development (HUD) funds free or very low-cost housing counseling nationwide. Housing counselors can help you understand the law and your options, organize your finances and represent you in negotiations with your lender, if you need this assistance. Find a HUD-approved housing counselor near you

7. Prioritize spending.

After healthcare, keeping your house should be your Number 1 priority. Review your income and expenses and see where you can cut spending. Look at canceling all unnecessary expenses that include eating out, cable TV, memberships, and entertainment that you can eliminate. Contact your credit cards to delay payments and other “unsecured” debt until you’re caught up on your mortgage payments.

8. Use your assets.

Do you have assets–a second car, jewelry, a whole life insurance policy–that you can sell for cash to help reinstate your loan? Can anyone in your household get an extra job to bring in additional income? Even if these efforts don’t significantly increase your available cash or your income, they demonstrate to your lender that you are willing to make sacrifices to keep your home.

9. Avoid foreclosure prevention companies.

You don’t need to pay fees for foreclosure prevention help–use that money to pay the mortgage instead. Many for-profit companies will contact you promising to negotiate with your lender. While these may be legitimate businesses, they will charge you a hefty fee (often two or three months’ mortgage payment) for information and services your lender or a HUD-approved housing counselor will provide free if you contact them.

10. Don’t lose your house to foreclosure recovery scams!

If any firm claims they can stop your foreclosure immediately and if you sign a document appointing them to act on your behalf, you may well be signing over the title to your property and becoming a renter in your own home! Never sign a legal document without reading and understanding all the terms and getting professional advice from an attorney, a trusted real estate professional or a HUD-approved housing counselor.

Few people think they will lose their home; they think they have more time.

Here’s how it happens. Note: Timeline varies by state.

- First month missed payment – your lender will contact you by letter or phone. A housing counselor can help.

- Second month missed payment – your lender is likely to begin calling you to discuss why you have not made your payments. It is important that you take their phone calls. Talk to your lender and explain your situation and what you are trying to do to resolve it. At this time, you still may be able to make one payment to prevent yourself from falling three months behind. A housing counselor can help.

- Third month missed payment after the third payment is missed, you will receive a letter from your lender stating the amount you are delinquent, and that you have 30 days to bring your mortgage current. This is called a “Demand Letter” or “Notice to Accelerate.” If you do not pay the specified amount or make some type of arrangements by the given date, the lender may begin foreclosure proceedings. They are unlikely to accept less than the total due without arrangements being made if you receive this letter. You still have time to work something out with your lender. A housing counselor can still help.

- Fourth month missed payment – now you are nearing the end of time allowed in your Demand or Notice to Accelerate Letter. When the 30 days ends, if you have not paid the full amount or worked our arrangements you will be referred to your lender’s attorneys. You will incur all attorney fees as part of your delinquency. A housing counselor can still help you.

- Sheriff’s or Public Trustee’s Sale – the attorney will schedule a Sale. This is the actual day of foreclosure. You may be notified of the date by mail, a notice is taped to your door, and the sale may be advertised in a local paper. The time between the Demand or Notice to Accelerate Letter and the actual Sale varies by state. In some states it can be as quick as 2-3 months. This is not the move-out date, but the end is near. You have until the date of sale to make arrangements with your lender, or pay the total amount owed, including attorney fees.

- Redemption Period – after the sale date, you may enter a redemption period. You will be notified of your time frame on the same notice that your state uses for your Sheriff’s or Public Trustee’s Sale.

Important: Stay in contact with your lender, and get assistance as early as possible. All dates are estimated and vary according to your state and your mortgage company.

Understand your rights.

Learn all that you can about your Florida mortgage rights and foreclosure laws. Review your loan documents to determine what your Flroida mortgage lender or servicer may do if you can’t make your payments. Review Florida laws, particularly Florida Statutes Chapter 702 to learn about foreclosure proceedings.

Contact a non-profit housing counselor.

Help and information are available to you free of cost. The HOPE NOW alliance provides a 24-hour hotline to provide mortgage counseling assistance in multiple languages. Reach this hotline by dialing, 1-888-995-HOPE. You may also obtain a list of U.S. Department of Housing and Urban Development (HUD) certified counselors in Florida here.

Understand the relevant terms.

If you are working with your mortgage servicer or an approved housing counselor to keep your home, there are several options:

- Reinstatement: Your servicer may agree to let you pay the total amount you are behind, in a lump sum payment and by a specific date. This is often combined with forbearance when you can show that funds from a bonus, tax refund or other source will become available at a specific time in the future. Be aware that there may be late fees and other costs associated with a reinstatement plan.

- Forbearance: Your servicer may offer a temporary reduction or suspension of your mortgage payments while you get back on your feet. Forbearance is often combined with a reinstatement or a repayment plan to pay off the missed or reduced mortgage payments. Please be aware that some forbearance plans require that you immediately pay back the missed payments in a lump sum at the end of the plan.

- Repayment Plan: This is an agreement that gives you a fixed amount of time to repay the amount you are behind by combining a portion of what is past due with your regular monthly payment. At the end of the repayment period you have gradually paid back the amount of your mortgage that was delinquent.

- Loan Modification: This is a written agreement between you and your mortgage servicer that permanently changes one or more of the original terms of your note to make the payments more affordable.

If you and your servicer agree that you cannot keep your home, there may still be options to avoid foreclosure:

- Short Payoff: If you can sell your house but the sale proceeds are less than the total amount you owe on your mortgage, your mortgage servicer may agree to a short payoff and write off the portion of your mortgage that exceeds the net proceeds from the sale.

- Deed-in-Lieu of Foreclosure: A deed-in-lieu of foreclosure is a cancellation of your mortgage if you voluntarily transfer title of your property to your mortgage servicer. Usually you must try to sell your home for its fair market value for at least 90 days before a mortgage company will consider this option. A deed-in-lieu of foreclosure may not be an option if there are other liens on the property, such as second mortgages, judgments from creditors or tax liens.

- Assumption: An assumption permits a qualified buyer to take over your mortgage debt and make the mortgage payments, even if the mortgage is non-assumable. As a result, you may be able to sell your property and avoid foreclosure.

- ReStop Foreclosure mortgage refinancing : While reStop Foreclosure mortgage refinancing is not necessarily a good option when facing foreclosure and can sometimes even be a predatory practice, there are instances where it may help. Talk to your servicer to see if reStop Foreclosure mortgage refinancing is an option for you.

Carefully examine your finances.

Can you cut spending on optional expenses or delay payments on credit cards or other unsecured debt until you have paid your mortgage? Do you have assets that you could sell to help reinstate your loan? Can anyone in the household get a second job to help with income? These efforts to manage your finances may help you find income to apply to your outstanding payments and will demonstrate to your servicer that you are willing to work on your finances and make sacrifices in order to keep your home.

Do not fall victim to a foreclosure recovery scam.

If any business or individual offers to help you stop foreclosure immediately by signing a document authorizing them to act on your behalf or to set up Stop Foreclosure mortgage refinancing , do not sign without consulting a professional (an attorney or HUD-approved counselor). This may be a trick to get you to sign over title to your home. You are then vulnerable to losing your home and all of your equity in your home to the so-called rescuer.

The Consumer Financial Protection Bureau also provides useful information in avoiding scams. You can access the CFPB’s website on how to avoid foreclosure rescue scams here.

Avoid for-profit foreclosure prevention or loss mitigation companies.

If you fall behind in your mortgage payments, many for-profit companies will contact you promising to help you avoid foreclosure. Some may even appear to be affiliated with your lender or servicer. It is best to avoid dealing with these companies. Most will charge you a hefty fee up front for information that your servicer or a HUD-approved counselor will provide for free. You can obtain the same plan or a better plan for free by contacting your servicer or a HUD-approved counselor. Use your money to pay the mortgage instead.

Should you require outside resources to avoid foreclosure, seek out a licensed mortgage broker or an attorney. You can verify a mortgage broker’s license on the Office of Financial Regulation’s website. A rescue firm or mortgage broker may never charge you up front. They may only charge you after you receive and accept a written offer for a loan or refinance contract.

494.00794 Right to cure high-cost Florida home loans

(2) GROUNDS FOR REINSTATEMENT.Florida Business Refinance Before any action filed to foreclose upon the home or other action is taken to seize or transfer ownership of the home, a notice of the right to cure the default must be delivered to the borrower at the address of the property upon which any security exists for the home loan by postage prepaid certified United States mail, return receipt requested, which notice is effective upon deposit in the United States mail, and shall inform the borrower:

Seek additional information.

Information regarding mortgage and foreclosure issues from the following resources may prove helpful during this time:

- CFPB on mortgages

- Making Home Affordable

- Federal Trade Commission (FTC) on homes and mortgages

- The Florida Office of Financial Regulation on loan modifications

Refinance To Stop Foreclosure All Florida:

| Alachua | Alachua County |

| Alford | Jackson County |

| Altamonte Springs | Seminole County |

| Altha | Calhoun County |

| Anna Maria | Manatee County |

| Apalachicola | Frankin County |

| Apopka | Orange County |

| Arcadia | DeSoto County |

| Archer | Alachua County |

| Astatula | Lake County |

| Atlantic Beach | Duval County |

| Atlantis | Palm Beach County |

| Auburndale | Polk County |

| Aventura | Miami-Dade County |

| Avon Park | Highlands County |

| Bal Harbor | Miami-Dade County |

| Baldwin | Duval County |

| Bartow | Polk County |

| Bascom | Jackson County |

| Bay Harbor Islands | Miami-Dade County |

| Bay Lake | Orange County |

| Bell | Gilchrist County |

| Belle Glade | Palm Beach County |

| Belle Isle | Orange County |

| Belleair | Pinellas County |

| Belleair Beach | Pinellas County |

| Belleair Bluffs | Pinellas County |

| Belleair Shore | Pinellas County |

| Belleview | Marion County |

| Beverly Beach | Flagler County |

| Biscayne Park | Miami-Dade County |

| Blountstown | Calhoun County |

| Boca Raton | Palm Beach County |

| Bonifay | Holmes County |

| Bonita Springs | Lee County |

| Bowling Green | Hardee County |

| Boynton Beach | Palm Beach County |

| Bradenton Beach | Manatee County |

| Bradenton | Manatee County |

| Branford | Suwannee County |

| Briny Breezes | Palm Beach County |

| Bristol | Liberty County |

| Bronson | Levy County |

| Brooker | Bradford County |

| Brooksville | Hernando County |

| Bunnell | Flagler County |

| Bushnell | Sumter County |

| Callahan | Nassau County |

| Callaway | Bay County |

| Cambelton | Jackson County |

| Cape Canaveral | Brevard County |

| Cape Coral | Lee County |

| Carrabelle | Frankin County |

| Caryville | Washington County |

| Casselberry | Seminole County |

| Cedar Grove | Bay County |

| Cedar Key | Levy County |

| Center Hill | Sumter County |

| Century | Escambia County |

| Chattahoochee | Gadsden County |

| Chiefland | Levy County |

| Chipley | Washington County |

| Cinco Bayou | Okaloosa County |

| Clearwater | Pinellas County |

| Clermont | Lake County |

| Clewiston | Hendry County |

| Cloud Lake | Palm Beach County |

| Cocoa | Brevard County |

| Cocoa Beach | Brevard County |

| Coconut Creek | Broward County |

| Coleman | Sumter County |

| Cooper City | Broward County |

| Coral Gables | Miami-Dade County |

| Coral Springs | Broward County |

| Cottondale | Jackson County |

| Crawfordville | Wakulla County |

| Crescent City | Putnam County |

| Crestview | Okaloosa County |

| Cross City | Dixie County |

| Crystal River | Citrus County |

| Dade City | Pasco County |

| Dania Beach | Broward County |

| Davenport | Polk County |

| Davie | Broward County |

| Daytona Beach | Volusia County |

| Daytona Beach Shores | Volusia County |

| DeBary | Volusia County |

| Deerfield Beach | Broward County |

| DeFuniak Springs | Walton County |

| DeLand | Volusia County |

| Delray Beach | Palm Beach County |

| Deltona | Volusia County |

| Destin | Okaloosa County |

| Doral | Miami-Dade County |

| Dundee | Polk County |

| Dunedin | Pinellas County |

| Dunnellon | Marion County |

| Eagle Lake | Polk County |

| Eatonville | Orange County |

| Ebro | Washington County |

| Edgewater | Volusia County |

| Edgewood | Orange County |

| El Portal | Miami-Dade County |

| Esto | Holmes County |

| Eustis | Lake County |

| Everglades City | Collier County |

| Fanning Springs* | Gilchrist County |

| Fanning Springs* | Levy County |

| Fellsmere | Indian River County |

| Fernandina Beach | Nassau County |

| Flagler Beach | Flagler County |

| Florida Bad Credit City | Miami-Dade County |

| Fort Lauderdale | Broward County |

| Fort Meade | Polk County |

| Fort Myers Beach | Lee County |

| Fort Myers | Lee County |

| Fort Pierce | St. Lucie County |

| Fort Walton Beach | Okaloosa County |

| Fort White | Columbia County |

| Freeport | Walton County |

| Frostproof | Polk County |

| Fruitland Park | Lake County |

| Gainesville | Alachua County |

| Glen Ridge | Palm Beach County |

| Glen Saint Mary | Baker County |

| Golden Beach | Miami-Dade County |

| Golf | Palm Beach County |

| Golfview | Palm Beach County |

| Graceville | Jackson County |

| Grand Ridge | Jackson County |

| Green Cove Springs | Clay County |

| Greenacres | Palm Beach County |

| Greensboro | Gadsden County |

| Greenvilee | Madison County |

| Greenwood | Jackson County |

| Gretna | Gadsden County |

| Groveland | Lake County |

| Gulf Breeze | Santa Rosa County |

| Gulf Stream | Palm Beach County |

| Gulfport | Pinellas County |

| Haines City | Polk County |

| Hallandale | Broward County |

| Hampton Beach | Bradford County |

| Hastings | St. Johns County |

| Havana | Gadsden County |

| Haverhill | Palm Beach County |

| Hawthorne | Alachua County |

| Hialeah | Miami-Dade County |

| Hialeah Gardens | Miami-Dade County |

| High Springs | Alachua County |

| Highland Beach | Palm Beach County |

| Highland Park | Polk County |

| Hillcrest Heights | Polk County |

| Hilliard | Nassau County |

| Hillsboro Beach | Broward County |

| Holly Hill | Volusia County |

| Hollywood | Broward County |

| Holmes Beach | Manatee County |

| Homestead | Miami-Dade County |

| Horseshoe Beach | Dixie County |

| Howey-in-the-Hills | Lake County |

| Hupoluxo | Palm Beach County |

| Indialantic | Brevard County |

| Indian Creek | Miami-Dade County |

| Indian Harbour Beach | Brevard County |

| Indian River Shores | Indian River County |

| Indian Rocks Beach | Pinellas County |

| Indian Shores | Pinellas County |

| Inglis | Levy County |

| Interlachen | Putnam County |

| Inverness | Citrus County |

| Islamorada | Monroe County |

| Islandia | Miami-Dade County |

| Jacksonville Beach | Duval County |

| Jacksonville | Duval County |

| Jacob | Jackson County |

| Jasper | Hamilton County |

| Jay | Santa Rosa County |

| Jennings | Hamilton County |

| Juno Beach | Palm Beach County |

| Jupiter | Palm Beach County |

| Jupiter Inlet Colony | Palm Beach County |

| Jupiter Island | Martin County |

| Kenneth City | Pinellas County |

| Key Biscayne | Miami-Dade County |

| Key Colony Beach | Monroe County |

| Key West | Monroe County |

| Keystone Heights | Clay County |

| Kissimmee | Osceola County |

| La Crosse | Alachua County |

| LaBelle | Hendry County |

| Lady Lake | Lake County |

| Lake Alfred | Polk County |

| Lake Buena Vista | Orange County |

| Lake Butler | Union County |

| Lake City | Columbia County |

| Lake Clarke Shores | Palm Beach County |

| Lake Hamilton | Polk County |

| Lake Helen | Volusia County |

| Lake Mary | Seminole County |

| Lake Park | Palm Beach County |

| Lake Placid | Highlands County |

| Lake Wales | Polk County |

| Lake Worth | Palm Beach County |

| Lakeland | Polk County |

| Lantana | Palm Beach County |

| Largo | Pinellas County |

| Lauderdale Lakes | Broward County |

| Lauderdale-by-the-Sea | Broward County |

| Lauderhill | Broward County |

| Laurel Hill | Okaloosa County |

| Lawtey | Bradford County |

| Layton | Monroe County |

| Lazy Lake | Broward County |

| Lee | Madison County |

| Leesburg | Lake County |

| Lighthouse Point | Broward County |

| Live Oak | Suwannee County |

| Longboat Key* | Sarasota County |

| Longboat Key* | Manatee County |

| Longwood | Seminole County |

| Lynn Haven | Bay County |

| Macclenny | Baker County |

| Madeira Beach | Pinellas County |

| Madison | Madison County |

| Maitland | Orange County |

| Malabar | Brevard County |

| Malone | Jackson County |

| Manalapan | Palm Beach County |

| Mangonia Park | Palm Beach County |

| Marathon | Monroe County |

| Marco Island | Collier County |

| Margate | Broward County |

| Marianna | Jackson County |

| Marineland* | St. Johns County |

| Marineland* | Flagler County |

| Mary Esther | Okaloosa County |

| Mascotte | Lake County |

| Mayo | Lafayette County |

| McIntosh | Marion County |

| Medley | Miami-Dade County |

| Melbourne | Brevard County |

| Melbourne Beach | Brevard County |

| Melbourne Village | Brevard County |

| Mexico Beach | Bay County |

| Miami Beach | Miami-Dade County |

| Miami Gardens | Miami-Dade County |

| Miami Lakes | Miami-Dade County |

| Miami Shores Village | Miami-Dade County |

| Miami Springs | Miami-Dade County |

| Miami, Florida, Bad Credit | Miami-Dade County |

| Micanopy | Alachua County |

| Midway | Gadsden County |

| Milton | Santa Rosa County |

| Minneola | Lake County |

| Miramar | Broward County |

| Monticello | Jefferson County |

| Montverde | Lake County |

| Moore Haven | Glades County |

| Mount Dora | Lake County |

| Mulberry | Polk County |

| Naples | Collier County |

| Neptune Beach | Duval County |

| New Port Richey | Pasco County |

| New Smyrna Beach | Volusia County |

| Newberry | Alachua County |

| Niceville | Okaloosa County |

| Noma | Holmes County |

| North Bay Village | Miami-Dade County |

| North Lauderdale | Broward County |

| North Miami | Miami-Dade County |

| North Miami Beach | Miami-Dade County |

| North Palm Beach | Palm Beach County |

| North Port | Sarasota County |

| North Redington Beach | Pinellas County |

| Oak Hill | Volusia County |

| Oakland | Orange County |

| Oakland Park | Broward County |

| Ocala | Marion County |

| Ocean Breeze Park | Martin County |

| Ocean Ridge | Palm Beach County |

| Ocoee | Orange County |

| Okeechobee | Okeechobee County |

| Oldsmar | Pinellas County |

| Opa-locka | Miami-Dade County |

| Orange City | Volusia County |

| Orange Park | Clay County |

| Orchid | Indian River County |

| Orlando | Orange County |

| Ormond Beach | Volusia County |

| Otter Creek | Levy County |

| Oviedo | Seminole County |

| Pahokee | Palm Beach County |

| Palatka | Putnam County |

| Palm Bay | Brevard County |

| Palm Beach | Palm Beach County |

| Palm Beach Shores | Palm Beach County |

| Palm Beach Gardens | Palm Beach County |

| Palm Coast | Flagler County |

| Palm Shores | Brevard County |

| Palm Springs | Palm Beach County |

| Palmetto | Manatee County |

| Palm Harbor | Pinellas County |

| Palmetto Bay | Miami-Dade County |

| Panama City | Bay County |

| Panama City Beach | Bay County |

| Parker | Bay County |

| Parkland | Broward County |

| Paxton | Walton County |

| Pembroke Park | Broward County |

| Pembroke Pines | Broward County |

| Penney Farms | Clay County |

| Pensacola | Escambia County |

| Perry | Taylor County |

| Pierson | Volusia County |

| Pine Crest | Miami-Dade County |

| Pinellas Park | Pinellas County |

| Plant City | Hillsborough County |

| Plantation | Broward County |

| Polk City | Polk County |

| Pomona Park | Putnam County |

| Pompano Beach | Broward County |

| Ponce De Leon | Holmes County |

| Ponce Inlet | Volusia County |

| Port Ornage | Volusia County |

| Port Richey | Pasco County |

| Port St. Lucie | St. Lucie County |

| Port St. Joe | Gulf County |

| Punta Gorda | Charlotte County |

| Quincy | Gadsden County |

| Raiford | Union County |

| Reddick | Marion County |

| Redington Beach | Pinellas County |

| Redington Shores | Pinellas County |

| Riviera Beach | Palm Beach County |

| Rockledge | Brevard County |

| Royal Palm Beach | Palm Beach County |

| Safety Harbor | Pinellas County |

| Saint Leo | Pasco County |

| San Antonio | Pasco County |

| Sanford | Seminole County |

| Sanibel | Lee County |

| Sarasota | Sarasota County |

| Satellite Beach | Brevard County |

| Sea Ranch Lakes | Broward County |

| Sebastian | Indian River County |

| Seabring | Highlands County |

| Seminole | Pinellas County |

| Sewall’s Point | Martin County |

| Shalimar | Okaloosa County |

| Sneads | Jackson County |

| Sopchoppy | Wakulla County |

| South Bay | Palm Beach County |

| South Daytona | Volusia County |

| Sounty Miami | Miami-Dade County |

| South Palm Beach | Palm Beach County |

| South Pasadena | Pinellas County |

| Southwest Ranches | Bay County |

| Springfield | Bay County |

| St. Augustine Beach | St. Johns County |

| St. Augustine | St. Johns County |

| St. Cloud | Osceola County |

| St. Lucie Village | St. Lucie County |

| St. Marks | Wakulla County |

| St. Pete Beach | Pinellas County |

| St. Petersburg | Pinellas County |

| Starke | Bradford County |

| Stuart | Martin County |

| Sun City Center | Hillsborough County |

| Sunny Hills | Washington County |

| Sunny Isles Beach | Miami-Dade County |

| Sunrise | Broward County |

| Surfside | Miami-Dade County |

| Sweetwater | Miami-Dade County |

| Tallahassee | Leon County |

| Tamarac | Broward County |

| Tampa | Hillsborough County |

| Tarpon Springs | Pinellas County |

| Tavares | Lake County |

| Temple Terrace | Hillsborough County |

| Tequesta | Palm Beach County |

| Titusville | Brevard County |

| Treasure Island | Pinellas County |

| Trenton | Gilchrist County |

| Umatilla | Lake County |

| Valpariso | Okaloosa County |

| Venice | Sarasota County |

| Vernon | Washington County |

| Vero Beach | Indian River County |

| Virginia Gardens | Miami-Dade County |

| Waldo | Alachua County |

| Wauchula | Hardee County |

| Wausau | Washington County |

| Webster | Sumter County |

| Weeki Wachee | Hernando County |

| Welaka | Putnam County |

| Wellington | Palm Beach County |

| West Melbourne | Brevard County |

| West Miami | Miami-Dade County |

| West Palm Beach | Palm Beach County |

| Weston | Broward County |

| Westville | Holmes County |

| Wewahitchka | Gulf County |

| White Springs | Hamilton County |

| Wildwood | Sumter County |

| Williston | Levy County |

| Wilton Manors | Broward County |

| Windermere | Orange County |

| Winter Garden | Orange County |

| Winter Haven | Polk County |

| Winter Park | Orange County |

| Winter Springs | Seminole County |

| Worthington Springs | Union County |

| Yankeetown | Levy County |

| Youngstown | Bay County |

| Zephyrhills | Pasco County |

| Zolfo Springs | Hardee County |