Non-Permanent Resident Florida Mortgage Lenders

Non-Permanent Resident Florida Mortgage Loan Options. If you are trying to buy a house in Florida as a non-permanent resident, our structured financing option might work for you. The non-resident Dream Builder program is a unique opportunity in which a purchase transaction is completed by an FHA-eligible government entity that enters into a lease-to-own and long-term purchase agreement, or structured financing agreement, with qualified non-resident Florida Homebuyers, thereby allowing the non-resident Homebuyers to purchase the property in the future. The Homebuyer(s) move into the property and begin their journey toward owning the home! • The option purchase price reduces with each monthly payment made by the Homebuyer(s). • All appreciation acquired from the date of closing until the Homebuyer(s) purchase the property belongs to the Homebuyer(s). • At any time, the Homebuyer(s) can sell the home, purchase the property from the FHA-eligible government entity, or assume the existing FHA loan on the property.

Non-Permanent Resident Florida Mortgage Lenders

Non-Resident Mortgage Program Overview

The NEW non-resident DreamBuilder program is a unique opportunity in which a purchase transaction is completed by an FHA-eligible government entity that enters into a lease-to-own and long-term purchase agreement, or structured financing agreement, with qualified non-resident Florida Homebuyers, thereby allowing the Homebuyers to lock in the price now, build equity and purchase the property in the future.

No Tax Return Florida Mortgage Option

Non-Resident Florida Mortgage Options

The Homebuyer(s) move into the property and begin their journey toward owning the home!

• The option purchase price reduces with each monthly payment made by the Homebuyer(s).

• All appreciation acquired from the date of closing until the Homebuyer(s) purchase the property belongs to the Homebuyer(s). • At any time, the non-resident Homebuyer(s) can

1) Sell the home,

2) Purchase the property from an FHA-eligible government entity, or

3) Assume the existing FHA loan on the property.

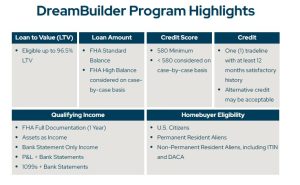

Eligibility

- Loan to Value – Eligible up to 96.5% LTV = 3.5% downpayment. Seller paid closing costs up to 6%.

- Loan Amount – FHA Standard Balance – FHA High Balance is considered on a case-by-case basis.

- Qualifying Income – Mix, Full Doc, Assets, 3 months Bank Statement, Only Income P&L + Bank Statements,1099s.

- Credit Score – 580 Minimum, One (1) tradeline with at least 12 months satisfactory history. Alternative credit ok.

- Homebuyer Eligibility– Non-Permanent Resident, including ITIN and DACA

Non-Permanent Resident Florida Mortgage

How Does The Program Work?

Non-Permanent Resident CONSUMER DISCLOSURE (“Originator”) desires to serve all consumers’ home financing needs, including those in typically underserved markets or those who may not qualify for traditional mortgage finance. With this mission in mind, Originator may refer certain consumers to the “Non-Permanent Resident Dreambuilder Program” (the “Program”). Originator works with an unaffiliated party to provide the Program as a bridge to homeownership for Florida Non-Permanent Residents for consumers unlikely to qualify for traditional conforming financing.It is important to understand, however, that the Program is not a mortgage loan offered by the Originator. The

The program is a shared ownership financing program to bridge the gap between renting and homeownership for A Non-Permanent Resident who may not qualify for a traditional mortgage. The basic structure of the Non-Permanent Resident Program is as follows for approved consumers (“Homebuyers”): • A governmental Agency (“Agency”) — often an affiliate of a Native American Tribe purchases a Florida home (“Home”) using the Non-Permanent Resident Homebuyers’ purchase and sale agreement with a third-party seller. • Originator lends funds to the Agency for the purchase of the Home. • The Agency enters into a ground lease financing agreement with Non-Permanent Resident Homebuyers to purchase the home and obtain a leasehold interest in the land (the “Homeownership Agreement”). • In addition to making the payments required by the Homeownership Agreement, Non-Permanent Resident Homebuyers must occupy and maintain the Home. • The Homeownership Agreement has an option to purchase the Home (the “Purchase Option”) and otherwise is amortized and fully paid over 40 years, similar to a fully amortizing mortgage. Highlighted Differences with Traditional Mortgage Finance. As stated above, the Homeownership Agreement is not a traditional mortgage loan. Some, but not all, differences between this Program and a traditional mortgage loan are detailed below. Again, please review the Homeownership Agreement for additional information before deciding to proceed: 1. The Homeownership Agreement is a financing arrangement whereby the Agency will own fee simple title to the Home until exercise of the Purchase Option or payment in full. 2. Non-Permanent Residents Homebuyers own the Home through a ground lease interest created by the Homeownership Agreement. A fee simple title is transferred to Non-Permanent Resident Homebuyers upon exercise of the Purchase Option or payment in full. The Non-Permanent Resident Homebuyers will be required to sign a release of personal information so Originator can send that information to the Agency. 4. The Agency may obtain property insurance under a master policy, or the Homebuyers may select the insurance provider. Homebuyers are responsible for insurance costs, which will be part of the monthly payment. 5. The Homebuyers do not receive a Loan Estimate of charges from the Originator. If approved for the Program, Non-Permanent Resident Homebuyers will get a summary of the monthly payment obligations and closing charges for the agreement. 6. Homebuyers are restricted from leasing, subletting or financing the Home, even for temporary uses. 7. Purchase or refinance requires payment of all applicable fees under the Homeownership Agreement. 8. The Homebuyers must have documented housing payment history. 9. Mandatory homeownership education courses may be required. 10. Delayed closing or occupancy may result in the voiding of any Agency commitment.

Non-Permanent Resident Disclosure

The Non-Permanent Resident DreamBuilder Program (the Program) is an alternative path to homeownership for

Non-Permanent Resident who may not qualify for traditional mortgage loans, but who want to lock in a home price today to begin building their generational wealth. Here is how it works:

• What is the Non-Permanent Resident DreamBuilder Program? The Non-Permanent Resident selects a home to buy that is within their monthly budget. Because they don’t qualify for a mortgage loan, the home is purchased by a governmental entity and the Non-Permanent Resident enters into a long-term Non-Permanent Resident homebuyer agreement that allows them to live in and enjoy the home with an option to take traditional title to the property when they are able to qualify for a traditional mortgage or pay the agreement in full. At any time during the contract period, the Non-Permanent Resident may exercise the right to take traditional title to the home. The Non-Permanent Resident has 40 years to take traditional ownership of the home by obtaining a new loan or by assuming the loan used by the government entity. As long as all payments are made as agreed, the Non-Permanent Resident receives all the benefits of home appreciation, and the amount owed under the agreement is paid down with each monthly payment, similar to a 40-year

amortized loan.

• How is a home selected? The Non-Permanent Resident selects a home that meets the Non-Permanent Resident’s needs and places an offer on the home. The purchase agreement signed by the Non-Permanent Resident on the home is transferred to a governmental agency associated with an Indian Tribe, the Tule River Homebuyer Earned Equity Agency (TRHEEA). TRHEEA buys the selected property using funds obtained through an FHA-insured first mortgage loan on the property and the fee paid by the Non-Permanent Resident when executing the Homebuyer

Agreement.

• What does the DreamBuilder Program cost? Upfront, the Non-Permanent Resident will pay a fee that covers the down payment and closing costs to purchase the home, plus program administration costs. Monthly payments include the principal, interest, and mortgage insurance paid on the FHA-insured loan, plus property taxes, hazard insurance, repairs, homeowner’s association dues, property maintenance, etc. An estimate of these costs is provided to the Non-Permanent Resident shortly after a home is selected and the final cost is determined, before signing the final agreement. Once the Non-Permanent Resident is ready and qualifies for mortgage financing, the government entity will allow the Non-Permanent Resident to either assume the FHA-insured loan from the government entity, or the Non-Permanent Resident can obtain their financing to pay the agreement in full.

• What are the advantages of the DreamBuilder Program? o Increases in the home’s value during the term of the agreement benefit the Non-Permanent Resident as long as all payments are made as agreed. (Of course, there is no guarantee that homes will go up in value; they can also go down in value.) o Each month, a portion of the monthly payment reduces the amount owed under the agreement to take traditional ownership in the home.

o By faithfully making the monthly payments and by paying the other expenses of owning a home a

Non-Permanent Resident demonstrates their ability to own a home and improves their likelihood of obtaining traditional financing.

o Under some circumstances, it may be possible for a Non-Permanent Resident to “assume” the mortgage obtained

by TRHEEA, which would avoid the need for the Non-Permanent Resident to obtain a new mortgage and save them

thousands of dollars in closing costs.

o If the Non-Permanent Resident decides not to purchase the home, there may be other options available, depending

on the circumstances: (1) work with TRHEEA to find someone to assume their obligations under the

Homebuyer Agreement; (2) sell the home and the Non-Permanent Resident receives all sales proceeds remaining

after the Homebuyer Agreement is paid in full and sales costs are paid; or (3) abandon the property

and cancel the agreement, placing the disposition of the home in the hands of TRHEEA. In this

option, no costs paid by the Non-Permanent Resident are refundable.

o A memorandum of the agreement is filed with the county records office assuring the Non-Permanent Resident ’s

rights under the agreements are protected as long as the regular monthly payments are made on

time.

• What are the requirements to qualify for the DreamBuilder Program?

o A financial application must be filled out by the Non-Permanent Resident and a credit report obtained.

o The Non-Permanent Resident must provide a well-documented ability to make monthly housing payments, including

the amount of the monthly payment and the costs of maintaining a home. An evaluation is made by

TRHEEA with assistance from Open Mortgage Wholesale of the Non-Permanent Resident’s financial ability to make

the monthly payments required by the agreement and the expenses of maintaining a home.

o Demonstrate the ability to pay the upfront costs required to consummate the Homebuyer

Agreement.

o If the Non-Permanent Resident’s financial ability is approved by TRHEEA, the normal real estate purchase process

is followed to select a home and obtain a purchase and sale contract on it. Earnest money is provided by the Non-Permanent Resident. That contract is assigned to TRHEEA.

o Consumer education courses may be required.

o The opportunity to buy the home can be lost if the Non-Permanent Resident fails to make monthly payments or violates any other terms of the Homebuyer Agreement.

o Delayed closing or occupancy of the property may result in failure to purchase the property and revocation of the Homebuyer Agreement.

Dream Builder Question Answers

Can the Non-Permanent Resident Homebuyer sell the property that is acquired through the DreamBuilder program?

• The Non-Permanent Resident Homebuyer may coordinate the property sale with the government entity (TRHEEA), provided all payments have been timely, the account is in good standing, and the underlying option price is satisfied in full with the property sale. Otherwise, the Non-Permanent Resident Homebuyer must meet all FHA guidelines and assume the FHA mortgage from the government entity, then the Homebuyer can sell the property after the assumption is complete.

Is the Non-Permanent Resident Homebuyer listed on the mortgage security instrument or note?

• No, the Homebuyer is not named on either legal document.

Can the Non-Permanent Resident Homebuyer refinance the DreamBuilder loan?

• The Homebuyer must first meet all FHA guidelines and assume the FHA mortgage from the government entity. The

Homebuyer can refinance the property after the assumption is completed.

Are seller concessions allowed for the DreamBuilder program?

• There are no overlays, refer to the HUD Handbook 4000.1.

Are all title companies approved for the DreamBuilder program?

• No, please refer to the DreamBuilder Approved Title Company list.

Does the Non-Permanent Resident’s DreamBuilder program have a restriction on the maximum number of Homebuyers for a transaction?

• Yes, no more than four (4) applications are permitted.

Is a non-occupant Homebuyer permitted?

• Yes, refer to the guidelines for details.

Does the Non-Permanent Resident DreamBuilder program allow exceptions?

• Yes, on a case-by-case basis. Refer to the exception parameters of the guidelines for details and requirements.

Can the Non-Permanent Resident Homebuyer make higher monthly payments to reduce the underlying option price and expedite the property transfer?

• Yes, this is acceptable. The Homebuyer must remit the standard monthly payment per the terms of the agreement via

ACH AND mail a separate check for the additional principal payment to the government entity (TRHEEA) with clear

Instructions in the check memo to apply the excess funds as a principal reduction.

Credit & Qualifying

Is a Homebuyer without a credit score acceptable?

• Yes, Homebuyers without a credit score may be acceptable, subject to the requirements of the guidelines.

What are the tradeline requirements for the DreamBuilder program?

• An eligible credit report must reflect at least one (1) tradeline and provide at least 12 months of credit history. Alternative tradeline history may be acceptable; refer to the guidelines for details.

What credit bureau is used to qualify for the DreamBuilder program?

• At least one (1) credit score from a major bureau is required to qualify. If the Homebuyer has multiple credit scores, the representative score will be the middle score when three (3) credit agency scores return and the lower score when two (2) credit agency scores return. Homebuyers without a credit score may be acceptable, subject to the requirements of the guidelines.

Are Homebuyers with no documented housing history eligible for the DreamBuilder program?

• Generally, 12 months of documented payment history (in good standing) is required. Homebuyers who live “rent free” may be considered on a case-by-case basis, refer to the guidelines.

If the Homebuyer owns their current residence free and clear, can the DreamBuilder housing payment history

Requirements be met with a documented history for other real estate owned by the Homebuyer?

• Yes, housing history for other real estate owned by the Homebuyer will be considered when the primary residence is

owned free and clear, subject to validation of reasonable occupancy for the subject property. Additionally, tax and

insurance payments for the primary residence will be considered to support consistent housing history.

What is required if the Homebuyer wants to rent their current primary (departure) residence or has an existing rental property?

• One (1) currently owned property (departure residence) may be allowed, subject to all requirements of the guidelines.

Rental income from an existing rental property may be considered on a case-by-case basis, refer to the guidelines for

details.

Do installment debts with less than 10 payments have to be included in the DTI?

• Yes, in some cases. Refer to the guidelines for details.

Can debt be paid off to qualify?

• Yes, the assets used for such payoffs must be documented per the guidelines.

If the Homebuyer has tax liens, collections, charge-off accounts, and/or judgments, how is the debt treated?

• Generally, tax liens and collection accounts must be included in the qualifying DTI. Refer to the guidelines for details.

• Debt payments for charge-off accounts and judgments are not required to be included in the qualifying DTI.

Is it acceptable to exclude self-reported utilities from the DTI?

• Yes. Utility payments are not required to be included in the qualifying DTI. Can co-signed debt be excluded from the Homebuyer’s qualifying DTI if documentation supports another party is paying the debt?

• There are no overlays, refer to the HUD Handbook 4000.1.

Income

Is the income for a self-employed Homebuyer without a business license permitted?

• May be acceptable on a case-by-case basis.

Will the loan be acceptable if the Social Security Number is different between the Homebuyer’s W-2 and

paystubs?

• Acceptable for ITIN Homebuyers and will be reviewed on a case-by-case basis for all other Homebuyer types.

Can bank statements be used to calculate income for a self-employed Homebuyer?

• The DreamBuilder program allows Homebuyers to qualify solely with three (3) months of bank statements when the

income source can only be documented with bank statements. For all other self-employed Homebuyers, the DreamBuilder program requires either prior year tax returns (filed with the IRS), OR a YTD P&L and three (3) months

of bank statements to document the business cash-flow, OR K1s and 1120s. Refer to the guidelines for details.

What is the minimum length of self-employment for self-employed income to be acceptable?

• One (1) year may be acceptable on a case-by-case basis.

Will the income for a self-employed Homebuyer be considered if the tax returns show little to no profit?

• In some cases, yes, as tax returns are not the only source to validate the Homebuyer’s self-employed income. As a

reminder, the DreamBuilder program requires either prior year tax returns (filed with the IRS), OR a YTD P&L and three

(3) months of bank statements to document the business cash-flow, OR K1s and 1120s. Refer to the guidelines for

details.

What is the age of documentation requirement for a Profit and Loss (P&L) Statement?

• The P&L must be completed for the most recent quarter as of the Note Date.

If the Homebuyer has more than a single job, for how long must the Homebuyer have the additional job(s) to allow

The income for qualifying?

• Less than two (2) years of concurrent employment may be considered on a case-by-case basis.

For employment transfers or relocations, what documentation is acceptable to verify future income?

• There are no overlays; refer to the HUD Handbook 4000.1.

Property

Are there property types allowed by FHA that are not permitted in the DreamBuilder program?

• Yes – the DreamBuilder program prohibits 3-4 units and cooperative properties.

Is the homeowner’s insurance selected by the Homebuyer?

• In some cases, the Homebuyer may select their own HO-3 insurance policy. However, there are instances in which the government entity will acquire homeowner’s insurance for the subject property and the Homebuyer has the option to obtain renter’s insurance. Refer to the guidelines for details.

Does the home inspection have to be completed by a specific entity?

• No, any licensed home inspector and/or home inspection that meets FHA requirements is acceptable.

Does the Non-Permanent Residents DreamBuilder program allow partial home and/or system inspections?

• No, a full home inspection is required.

Who is responsible for verifying that the repairs required by a home inspection were completed?

• Generally, the appraisal must be completed in accordance with FHA guidelines. If the appraisal was completed “subject to”, a 1004D/Completion Certificate is required to confirm the completion of repairs.

Can the Homebuyer make modifications and/or renovations to the property after closing?

• This may be acceptable, subject to approval by the government entity. The Homebuyer must contact the government

entity (TRHEEA) to obtain a “Remodeling Request” form and initiate the property change approval process. The Homebuyer must submit the fully completed form to the government entity AND receive approval from The entity before making changes to the property

Non-Permanent Resident Florida Service Areas

| Alachua | Alachua County |

| Alford | Jackson County |

| Altamonte Springs | Seminole County |

| Altha | Calhoun County |

| Anna Maria | Manatee County |

| Apalachicola | Frankin County |

| Apopka | Orange County |

| Arcadia | DeSoto County |

| Archer | Alachua County |

| Astatula | Lake County |

| Atlantic Beach | Duval County |

| Atlantis | Palm Beach County |

| Auburndale | Polk County |

| Aventura | Miami-Dade County |

| Avon Park | Highlands County |

| Bal Harbor | Miami-Dade County |

| Baldwin | Duval County |

| Bartow | Polk County |

| Bascom | Jackson County |

| Bay Harbor Islands | Miami-Dade County |

| Bay Lake | Orange County |

| Bell | Gilchrist County |

| Belle Glade | Palm Beach County |

| Belle Isle | Orange County |

| Belleair | Pinellas County |

| Belleair Beach | Pinellas County |

| Belleair Bluffs | Pinellas County |

| Belleair Shore | Pinellas County |

| Belleview | Marion County |

| Beverly Beach | Flagler County |

| Biscayne Park | Miami-Dade County |

| Blountstown | Calhoun County |

| Boca Raton | Palm Beach County |

| Bonifay | Holmes County |

| Bonita Springs | Lee County |

| Bowling Green | Hardee County |

| Boynton Beach | Palm Beach County |

| Bradenton Beach | Manatee County |

| Bradenton | Manatee County |

| Branford | Suwannee County |

| Briny Breezes | Palm Beach County |

| Bristol | Liberty County |

| Bronson | Levy County |

| Brooker | Bradford County |

| Brooksville | Hernando County |

| Bunnell | Flagler County |

| Bushnell | Sumter County |

| Callahan | Nassau County |

| Callaway | Bay County |

| Cambelton | Jackson County |

| Cape Canaveral | Brevard County |

| Cape Coral | Lee County |

| Carrabelle | Frankin County |

| Caryville | Washington County |

| Casselberry | Seminole County |

| Cedar Grove | Bay County |

| Cedar Key | Levy County |

| Center Hill | Sumter County |

| Century | Escambia County |

| Chattahoochee | Gadsden County |

| Chiefland | Levy County |

| Chipley | Washington County |

| Cinco Bayou | Okaloosa County |

| Clearwater | Pinellas County |

| Clermont | Lake County |

| Clewiston | Hendry County |

| Cloud Lake | Palm Beach County |

| Cocoa | Brevard County |

| Cocoa Beach | Brevard County |

| Coconut Creek | Broward County |

| Coleman | Sumter County |

| Cooper City | Broward County |

| Coral Gables | Miami-Dade County |

| Coral Springs | Broward County |

| Cottondale | Jackson County |

| Crawfordville | Wakulla County |

| Crescent City | Putnam County |

| Crestview | Okaloosa County |

| Cross City | Dixie County |

| Crystal River | Citrus County |

| Dade City | Pasco County |

| Dania Beach | Broward County |

| Davenport | Polk County |

| Davie | Broward County |

| Daytona Beach | Volusia County |

| Daytona Beach Shores | Volusia County |

| DeBary | Volusia County |

| Deerfield Beach | Broward County |

| DeFuniak Springs | Walton County |

| DeLand | Volusia County |

| Delray Beach | Palm Beach County |

| Deltona | Volusia County |

| Destin | Okaloosa County |

| Doral | Miami-Dade County |

| Dundee | Polk County |

| Dunedin | Pinellas County |

| Dunnellon | Marion County |

| Eagle Lake | Polk County |

| Eatonville | Orange County |

| Ebro | Washington County |

| Edgewater | Volusia County |

| Edgewood | Orange County |

| El Portal | Miami-Dade County |

| Esto | Holmes County |

| Eustis | Lake County |

| Everglades City | Collier County |

| Fanning Springs | Gilchrist County |

| Fanning Springs | Levy County |

| Fellsmere | Indian River County |

| Fernandina Beach | Nassau County |

| Flagler Beach | Flagler County |

| Florida City | Miami-Dade County |

| Fort Lauderdale | Broward County |

| Fort Meade | Polk County |

| Fort Myers Beach | Lee County |

| Fort Myers | Lee County |

| Fort Pierce | St. Lucie County |

| Fort Walton Beach | Okaloosa County |

| Fort White | Columbia County |

| Freeport | Walton County |

| Frostproof | Polk County |

| Fruitland Park | Lake County |

| Gainesville | Alachua County |

| Glen Ridge | Palm Beach County |

| Glen Saint Mary | Baker County |

| Golden Beach | Miami-Dade County |

| Golf | Palm Beach County |

| Golfview | Palm Beach County |

| Graceville | Jackson County |

| Grand Ridge | Jackson County |

| Green Cove Springs | Clay County |

| Greenacres | Palm Beach County |

| Greensboro | Gadsden County |

| Greenvilee | Madison County |

| Greenwood | Jackson County |

| Gretna | Gadsden County |

| Groveland | Lake County |

| Gulf Breeze | Santa Rosa County |

| Gulf Stream | Palm Beach County |

| Gulfport | Pinellas County |

| Haines City | Polk County |

| Hallandale | Broward County |

| Hampton Beach | Bradford County |

| Hastings | St. Johns County |

| Havana | Gadsden County |

| Haverhill | Palm Beach County |

| Hawthorne | Alachua County |

| Hialeah | Miami-Dade County |

| Hialeah Gardens | Miami-Dade County |

| High Springs | Alachua County |

| Highland Beach | Palm Beach County |

| Highland Park | Polk County |

| Hillcrest Heights | Polk County |

| Hilliard | Nassau County |

| Hillsboro Beach | Broward County |

| Holly Hill | Volusia County |

| Hollywood | Broward County |

| Holmes Beach | Manatee County |

| Homestead | Miami-Dade County |

| Horseshoe Beach | Dixie County |

| Howey-in-the-Hills | Lake County |

| Hupoluxo | Palm Beach County |

| Indialantic | Brevard County |

| Indian Creek | Miami-Dade County |

| Indian Harbour Beach | Brevard County |

| Indian River Shores | Indian River County |

| Indian Rocks Beach | Pinellas County |

| Indian Shores | Pinellas County |

| Inglis | Levy County |

| Interlachen | Putnam County |

| Inverness | Citrus County |

| Islamorada | Monroe County |

| Islandia | Miami-Dade County |

| Jacksonville Beach | Duval County |

| Jacksonville | Duval County |

| Jacob | Jackson County |

| Jasper | Hamilton County |

| Jay | Santa Rosa County |

| Jennings | Hamilton County |

| Juno Beach | Palm Beach County |

| Jupiter | Palm Beach County |

| Jupiter Inlet Colony | Palm Beach County |

| Jupiter Island | Martin County |

| Kenneth City | Pinellas County |

| Key Biscayne | Miami-Dade County |

| Key Colony Beach | Monroe County |

| Key West | Monroe County |

| Keystone Heights | Clay County |

| Kissimmee | Osceola County |

| La Crosse | Alachua County |

| LaBelle | Hendry County |

| Lady Lake | Lake County |

| Lake Alfred | Polk County |

| Lake Buena Vista | Orange County |

| Lake Butler | Union County |

| Lake City | Columbia County |

| Lake Clarke Shores | Palm Beach County |

| Lake Hamilton | Polk County |

| Lake Helen | Volusia County |

| Lake Mary | Seminole County |

| Lake Park | Palm Beach County |

| Lake Placid | Highlands County |

| Lake Wales | Polk County |

| Lake Worth | Palm Beach County |

| Lakeland | Polk County |

| Lantana | Palm Beach County |

| Largo | Pinellas County |

| Lauderdale Lakes | Broward County |

| Lauderdale-by-the-Sea | Broward County |

| Lauderhill | Broward County |

| Laurel Hill | Okaloosa County |

| Lawtey | Bradford County |

| Layton | Monroe County |

| Lazy Lake | Broward County |

| Lee | Madison County |

| Leesburg | Lake County |

| Lighthouse Point | Broward County |

| Live Oak | Suwannee County |

| Longboat Key | Sarasota County |

| Longboat Key | Manatee County |

| Longwood | Seminole County |

| Lynn Haven | Bay County |

| Macclenny | Baker County |

| Madeira Beach | Pinellas County |

| Madison | Madison County |

| Maitland | Orange County |

| Malabar | Brevard County |

| Malone | Jackson County |

| Manalapan | Palm Beach County |

| Mangonia Park | Palm Beach County |

| Marathon | Monroe County |

| Marco Island | Collier County |

| Margate | Broward County |

| Marianna | Jackson County |

| Marineland | St. Johns County |

| Marineland | Flagler County |

| Mary Esther | Okaloosa County |

| Mascotte | Lake County |

| Mayo | Lafayette County |

| McIntosh | Marion County |

| Medley | Miami-Dade County |

| Melbourne | Brevard County |

| Melbourne Beach | Brevard County |

| Melbourne Village | Brevard County |

| Mexico Beach | Bay County |

| Miami Beach | Miami-Dade County |

| Miami Gardens | Miami-Dade County |

| Miami Lakes | Miami-Dade County |

| Miami Shores Village | Miami-Dade County |

| Miami Springs | Miami-Dade County |

| Miami | Miami-Dade County |

| Micanopy | Alachua County |

| Midway | Gadsden County |

| Milton | Santa Rosa County |

| Minneola | Lake County |

| Miramar | Broward County |

| Monticello | Jefferson County |

| Montverde | Lake County |

| Moore Haven | Glades County |

| Mount Dora | Lake County |

| Mulberry | Polk County |

| Naples | Collier County |

| Neptune Beach | Duval County |

| New Port Richey | Pasco County |

| New Smyrna Beach | Volusia County |

| Newberry | Alachua County |

| Niceville | Okaloosa County |

| Noma | Holmes County |

| North Bay Village | Miami-Dade County |

| North Lauderdale | Broward County |

| North Miami | Miami-Dade County |

| North Miami Beach | Miami-Dade County |

| North Palm Beach | Palm Beach County |

| North Port | Sarasota County |

| North Redington Beach | Pinellas County |

| Oak Hill | Volusia County |

| Oakland | Orange County |

| Oakland Park | Broward County |

| Ocala | Marion County |

| Ocean Breeze Park | Martin County |

| Ocean Ridge | Palm Beach County |

| Ocoee | Orange County |

| Okeechobee | Okeechobee County |

| Oldsmar | Pinellas County |

| Opa-locka | Miami-Dade County |

| Orange City | Volusia County |

| Orange Park | Clay County |

| Orchid | Indian River County |

| Orlando | Orange County |

| Ormond Beach | Volusia County |

| Otter Creek | Levy County |

| Oviedo | Seminole County |

| Pahokee | Palm Beach County |

| Palatka | Putnam County |

| Palm Bay | Brevard County |

| Palm Beach | Palm Beach County |

| Palm Beach Shores | Palm Beach County |

| Palm Beach Gardens | Palm Beach County |

| Palm Coast | Flagler County |

| Palm Shores | Brevard County |

| Palm Springs | Palm Beach County |

| Palmetto | Manatee County |

| Palm Harbor | Pinellas County |

| Palmetto Bay | Miami-Dade County |

| Panama City | Bay County |

| Panama City Beach | Bay County |

| Parker | Bay County |

| Parkland | Broward County |

| Paxton | Walton County |

| Pembroke Park | Broward County |

| Pembroke Pines | Broward County |

| Penney Farms | Clay County |

| Pensacola | Escambia County |

| Perry | Taylor County |

| Pierson | Volusia County |

| Pine Crest | Miami-Dade County |

| Pinellas Park | Pinellas County |

| Plant City | Hillsborough County |

| Plantation | Broward County |

| Polk City | Polk County |

| Pomona Park | Putnam County |

| Pompano Beach | Broward County |

| Ponce De Leon | Holmes County |

| Ponce Inlet | Volusia County |

| Port Ornage | Volusia County |

| Port Richey | Pasco County |

| Port St. Lucie | St. Lucie County |

| Port St. Joe | Gulf County |

| Punta Gorda | Charlotte County |

| Quincy | Gadsden County |

| Raiford | Union County |

| Reddick | Marion County |

| Redington Beach | Pinellas County |

| Redington Shores | Pinellas County |

| Riviera Beach | Palm Beach County |

| Rockledge | Brevard County |

| Royal Palm Beach | Palm Beach County |

| Safety Harbor | Pinellas County |

| Saint Leo | Pasco County |

| San Antonio | Pasco County |

| Sanford | Seminole County |

| Sanibel | Lee County |

| Sarasota | Sarasota County |

| Satellite Beach | Brevard County |

| Sea Ranch Lakes | Broward County |

| Sebastian | Indian River County |

| Seabring | Highlands County |

| Seminole | Pinellas County |

| Sewall’s Point | Martin County |

| Shalimar | Okaloosa County |

| Sneads | Jackson County |

| Sopchoppy | Wakulla County |

| South Bay | Palm Beach County |

| South Daytona | Volusia County |

| Sounty Miami | Miami-Dade County |

| South Palm Beach | Palm Beach County |

| South Pasadena | Pinellas County |

| Southwest Ranches | Bay County |

| Springfield | Bay County |

| St. Augustine Beach | St. Johns County |

| St. Augustine | St. Johns County |

| St. Cloud | Osceola County |

| St. Lucie Village | St. Lucie County |

| St. Marks | Wakulla County |

| St. Pete Beach | Pinellas County |

| St. Petersburg | Pinellas County |

| Starke | Bradford County |

| Stuart | Martin County |

| Sun City Center | Hillsborough County |

| Sunny Hills | Washington County |

| Sunny Isles Beach | Miami-Dade County |

| Sunrise | Broward County |

| Surfside | Miami-Dade County |

| Sweetwater | Miami-Dade County |

| Tallahassee | Leon County |

| Tamarac | Broward County |

| Tampa | Hillsborough County |

| Tarpon Springs | Pinellas County |

| Tavares | Lake County |

| Temple Terrace | Hillsborough County |

| Tequesta | Palm Beach County |

| Titusville | Brevard County |

| Treasure Island | Pinellas County |

| Trenton | Gilchrist County |

| Umatilla | Lake County |

| Valpariso | Okaloosa County |

| Venice | Sarasota County |

| Vernon | Washington County |

| Vero Beach | Indian River County |

| Virginia Gardens | Miami-Dade County |

| Waldo | Alachua County |

| Wauchula | Hardee County |

| Wausau | Washington County |

| Webster | Sumter County |

| Weeki Wachee | Hernando County |

| Welaka | Putnam County |

| Wellington | Palm Beach County |

| West Melbourne | Brevard County |

| West Miami | Miami-Dade County |

| West Palm Beach | Palm Beach County |

| Weston | Broward County |

| Westville | Holmes County |

| Wewahitchka | Gulf County |

| White Springs | Hamilton County |

| Wildwood | Sumter County |

| Williston | Levy County |

| Wilton Manors | Broward County |

| Windermere | Orange County |

| Winter Garden | Orange County |

| Winter Haven | Polk County |

| Winter Park | Orange County |

| Winter Springs | Seminole County |

| Worthington Springs | Union County |

| Yankeetown | Levy County |

| Youngstown | Bay County |

| Zephyrhills | Pasco County |

| Zolfo Springs | Hardee County |